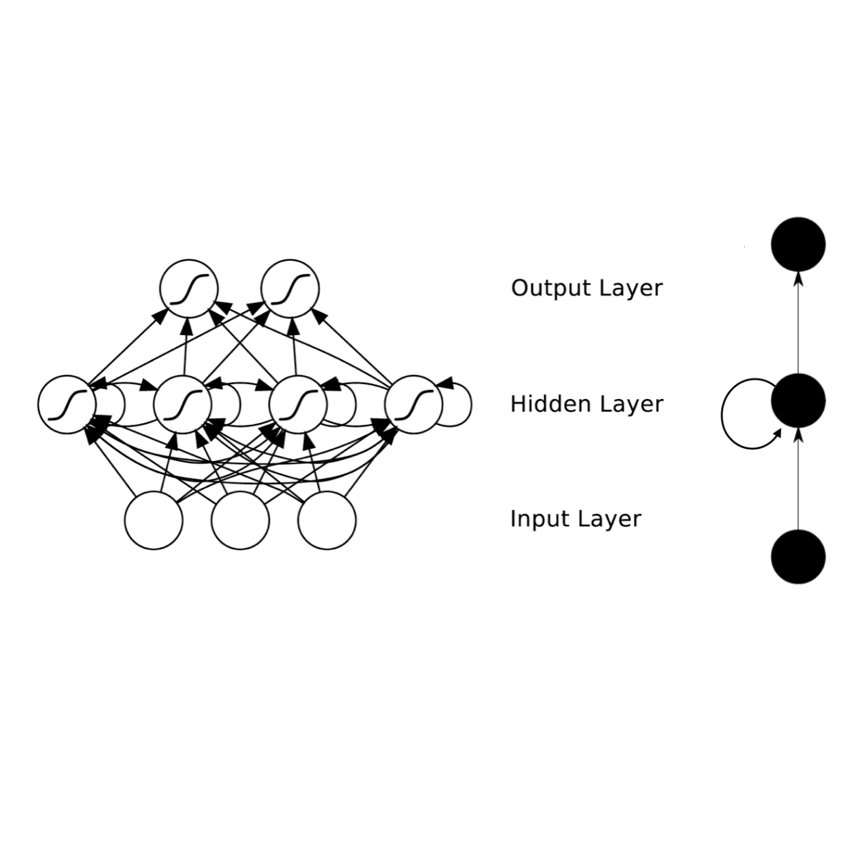

The Stochastic Volatility (SV) model and its variants are widely used in the financial sector while recurrent neural network (RNN) models are successfully used in many large-scale industrial applications of Deep Learning. Our article combines these two methods in a non-trivial way and proposes a model, which we call the Statistical Recurrent Stochastic Volatility (SR-SV) model, to capture the dynamics of stochastic volatility. The proposed model is able to capture complex volatility effects (e.g., non-linearity and long-memory auto-dependence) overlooked by the conventional SV models, is statistically interpretable and has an impressive out-of-sample forecast performance. These properties are carefully discussed and illustrated through extensive simulation studies and applications to five international stock index datasets: The German stock index DAX30, the Hong Kong stock index HSI50, the France market index CAC40, the US stock market index SP500 and the Canada market index TSX250. An user-friendly software package together with the examples reported in the paper are available at \url{https://github.com/vbayeslab}.

翻译:软体挥发性(SV)模型及其变体在金融部门广泛使用,而经常神经网络(RNN)模型在深层学习的许多大规模工业应用中被成功使用,我们的文章以非三边方式将这两种方法结合起来,并提出了一个模型,我们称之为统计经常性软体挥发性(SR-SV)模型,以捕捉随机挥发性(SV)的动态。拟议的模型能够捕捉常规的SV模型所忽视的复杂挥发性效应(例如非线性和长期模拟自动依赖性),在统计上是可以解释的,并且有一个令人印象深刻的标本以外的预测性能。通过广泛的模拟研究以及五个国际股票指数数据集的应用,对这些特性进行了认真讨论和说明:德国股票指数DAX30,香港股票指数HSI50,法国市场指数CAC40,美国股票市场指数SP500和加拿大市场指数TSX250。一个方便用户使用的软件包,以及本文所报告的例子,可在以下网址上查阅:http\ursmusbus/givlabbbbrea。