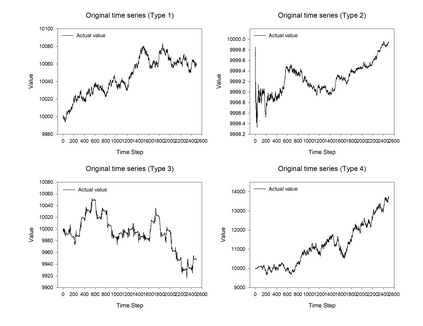

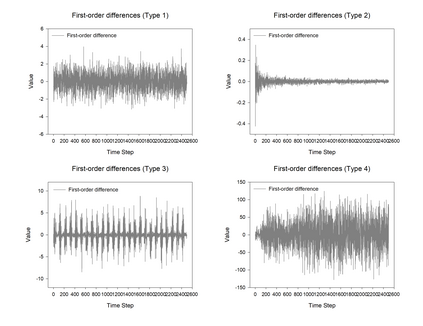

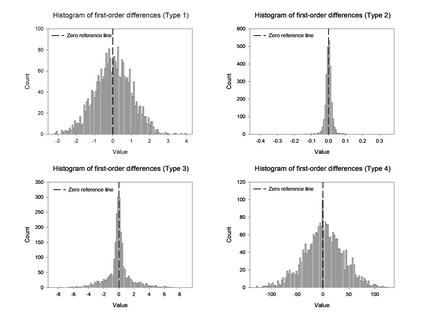

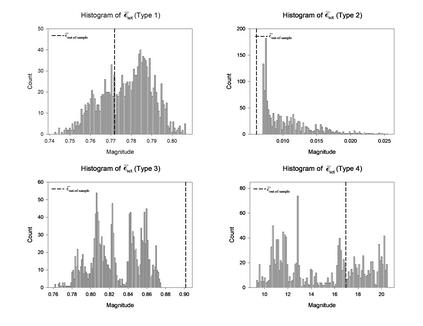

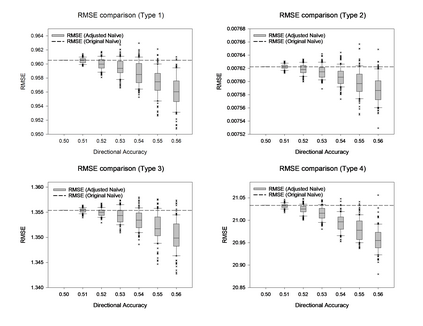

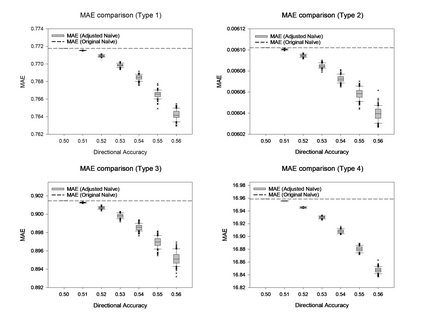

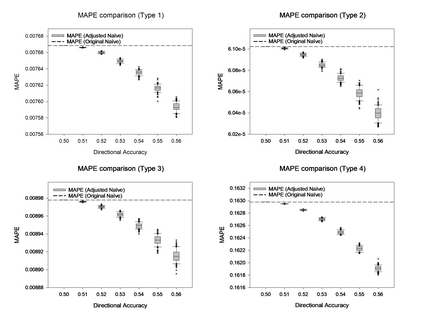

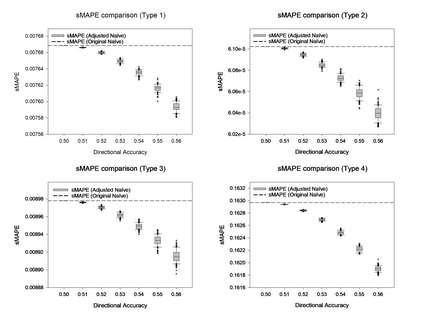

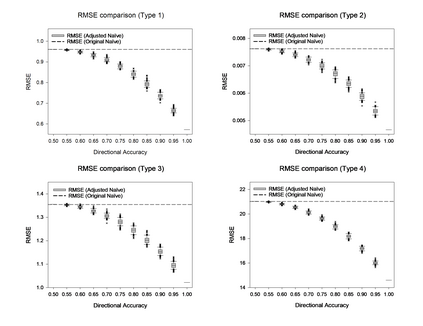

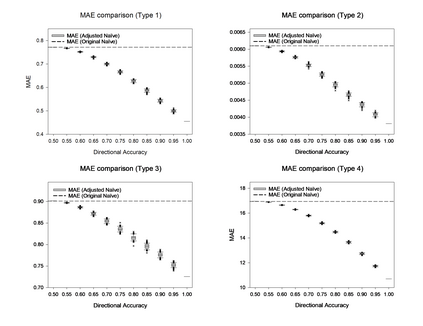

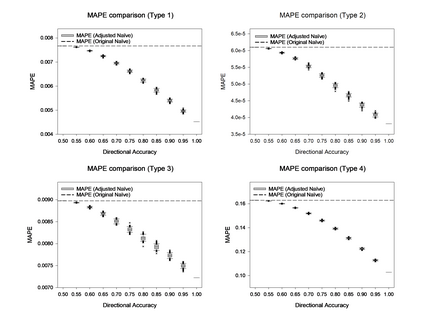

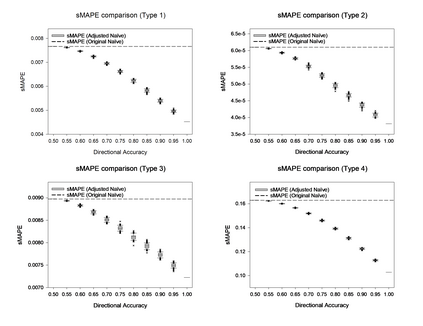

This study introduces a movement-prediction-adjusted na\"ive forecast, which is the original na\"ive forecast with the addition of a weighted movement prediction term, in the context of forecasting time series that exhibit symmetric random walk properties. The weight of the movement term is determined by two parameters: one reflecting the directional accuracy and the other representing the mean absolute increment. The settings of the two parameters involve a trade-off: larger values may yield meaningful gains over the original na\"ive forecast, whereas smaller values often render the adjusted forecast more reliable. This trade-off can be managed by empirically setting the parameters using sliding windows on in-sample data. To statistically test the performance of the adjusted na\"ive forecast under different directional accuracy levels, we used four synthetic time series to simulate multiple forecast scenarios, assuming that for each directional accuracy level, diverse movement predictions were provided. The simulation results show that as the directional accuracy increases, the error of the adjusted na\"ive forecast decreases. In particular, the adjusted na\"ive forecast achieves statistically significant improvements over the original na\"ive forecast, even under a low directional accuracy of slightly above 0.50. This finding implies that the movement-prediction-adjusted na\"ive forecast can serve as a new optimal point forecast for time series with symmetric random walk characteristics if consistent movement prediction can be provided.

翻译:暂无翻译