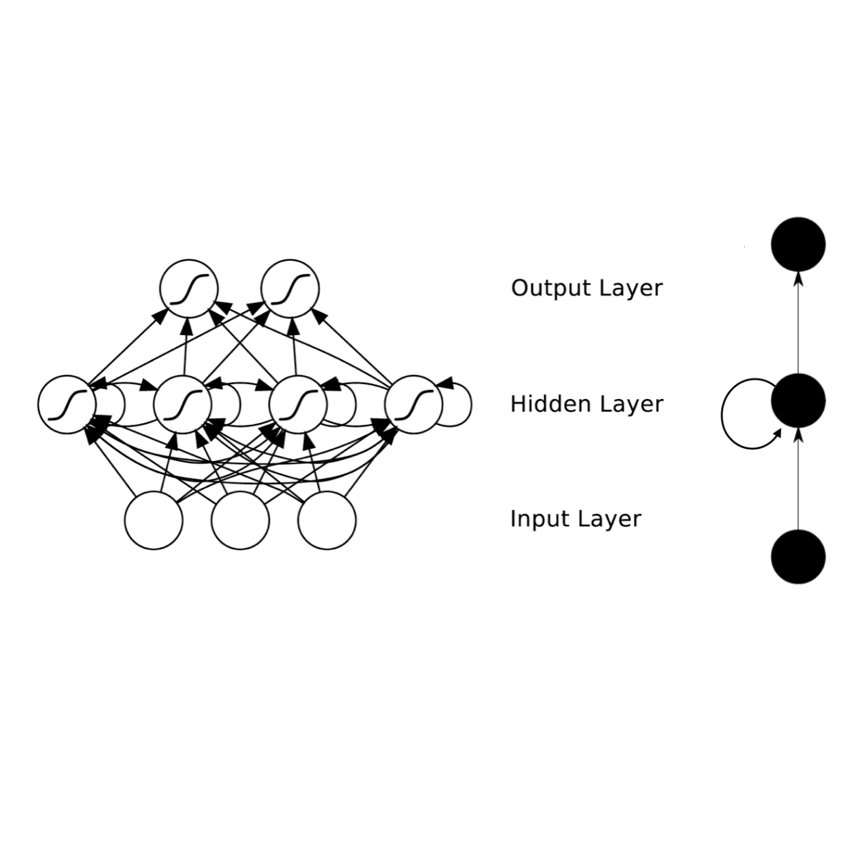

Time series forecasting based on deep architectures has been gaining popularity in recent years due to their ability to model complex non-linear temporal dynamics. The recurrent neural network is one such model capable of handling variable-length input and output. In this paper, we leverage recent advances in deep generative models and the concept of state space models to propose a stochastic adaptation of the recurrent neural network for multistep-ahead time series forecasting, which is trained with stochastic gradient variational Bayes. In our model design, the transition function of the recurrent neural network, which determines the evolution of the hidden states, is stochastic rather than deterministic as in a regular recurrent neural network; this is achieved by incorporating a latent random variable into the transition process which captures the stochasticity of the temporal dynamics. Our model preserves the architectural workings of a recurrent neural network for which all relevant information is encapsulated in its hidden states, and this flexibility allows our model to be easily integrated into any deep architecture for sequential modelling. We test our model on a wide range of datasets from finance to healthcare; results show that the stochastic recurrent neural network consistently outperforms its deterministic counterpart.

翻译:基于深层结构的时间序列预测近年来越来越受欢迎,因为它们有能力模拟复杂的非线性时间动态。 经常性神经网络是能够处理可变长度输入和输出的模型之一。 在本文中,我们利用最近深层基因模型的进展和国家空间模型的概念来提出对经常性神经网络进行多步头时间序列预测的随机调整,该神经网络经过了对梯度梯度变化波段的培训。 在我们的模型设计中,决定隐藏状态演变的经常性神经网络的过渡功能是随机的,而不是确定性的,就像在经常性经常性神经网络中那样;这是通过将潜在的随机变量纳入过渡进程来实现的。我们模型保存了一个经常性神经网络的建筑工作,所有相关信息都被封存在其隐藏状态中,这种灵活性使我们的模型很容易融入任何深层的序列建模结构。我们测试了从金融到卫生保健的广泛数据集的模型;其结果显示,其反复的神经网络具有稳定性。