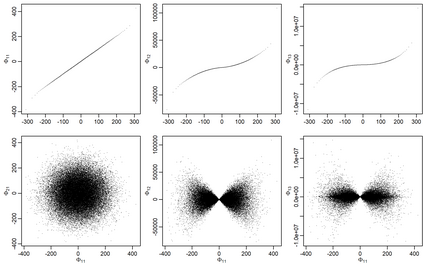

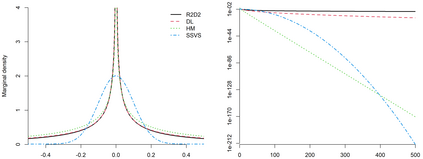

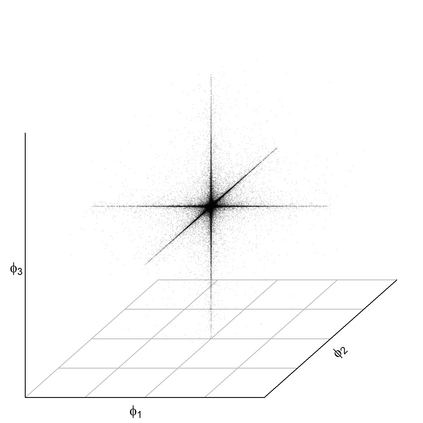

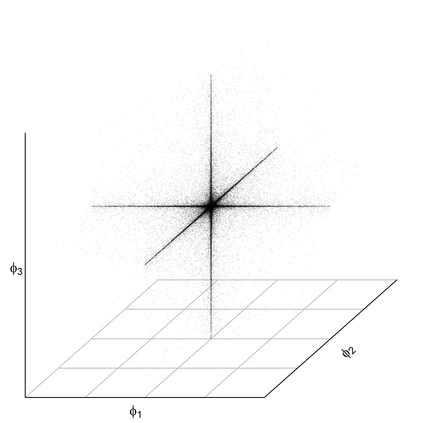

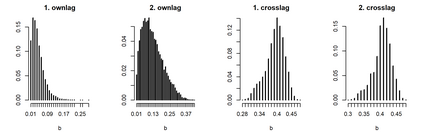

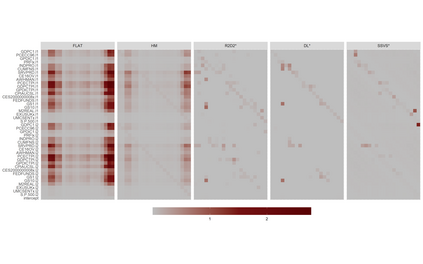

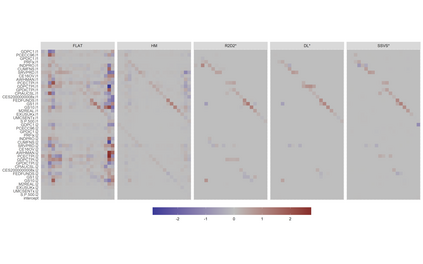

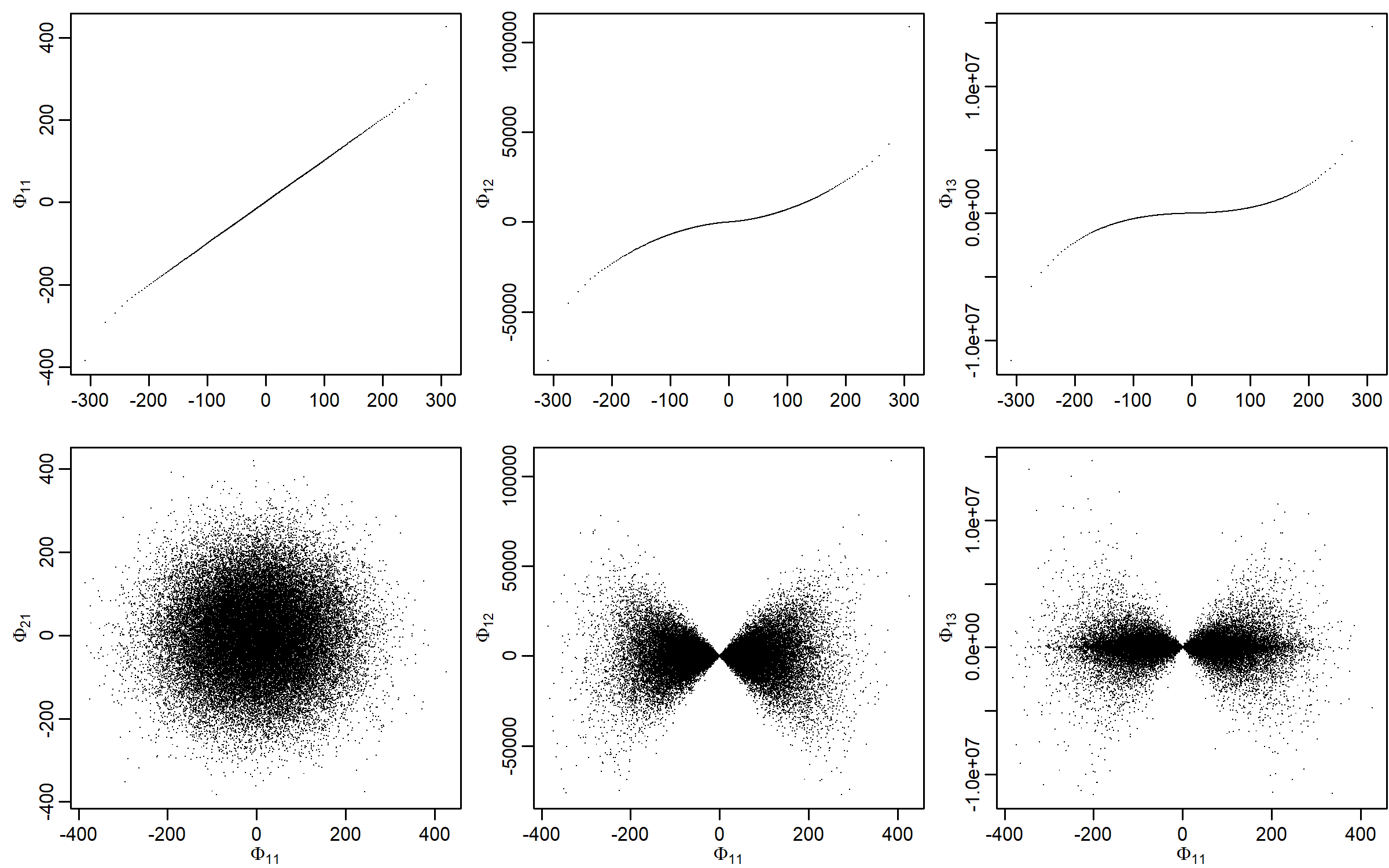

Vectorautogressions (VARs) are widely applied when it comes to modeling and forecasting macroeconomic variables. In high dimensions, however, they are prone to overfitting. Bayesian methods, more concretely shrinking priors, have shown to be successful in improving prediction performance. In the present paper we introduce the recently developed $R^2$-induced Dirichlet-decomposition prior to the VAR framework and compare it to refinements of well-known priors in the VAR literature. We demonstrate the virtues of the proposed prior in an extensive simulation study and in an empirical application forecasting data of the US economy. Further, we shed more light on the ongoing Illusion of Sparsity debate. We find that forecasting performances under sparse/dense priors vary across evaluated economic variables and across time frames; dynamic model averaging, however, can combine the merits of both worlds. All priors are implemented using the reduced-form VAR and all models feature stochastic volatility in the variance-covariance matrix.

翻译:在模拟和预测宏观经济变量时,矢量反射(VARs)被广泛应用,但在高维方面,这些变量容易被过度使用。巴伊西亚方法,更具体的缩水前期方法,在改善预测性能方面证明是成功的。在本文件中,我们介绍了最近在VAR框架之前开发的2美元引起的二氧化二氮分解,并将其与VAR文献中众所周知的前科的完善情况进行比较。我们在广泛的模拟研究中以及在美国经济的经验应用预测数据中,展示了先前提议的优点。此外,我们更清楚地介绍了正在进行的对种族分化辩论的幻觉。我们发现,在经过评估的经济变量和跨时间框架之间,在稀少/大量前期的预测性能各不相同;但是,平均动态模型可以将两个世界的优点结合起来。所有前期模型都使用缩小型VAR和所有模型在差异变异矩阵中具有随机性波动性。

相关内容

- Today (iOS and OS X): widgets for the Today view of Notification Center

- Share (iOS and OS X): post content to web services or share content with others

- Actions (iOS and OS X): app extensions to view or manipulate inside another app

- Photo Editing (iOS): edit a photo or video in Apple's Photos app with extensions from a third-party apps

- Finder Sync (OS X): remote file storage in the Finder with support for Finder content annotation

- Storage Provider (iOS): an interface between files inside an app and other apps on a user's device

- Custom Keyboard (iOS): system-wide alternative keyboards

Source: iOS 8 Extensions: Apple’s Plan for a Powerful App Ecosystem