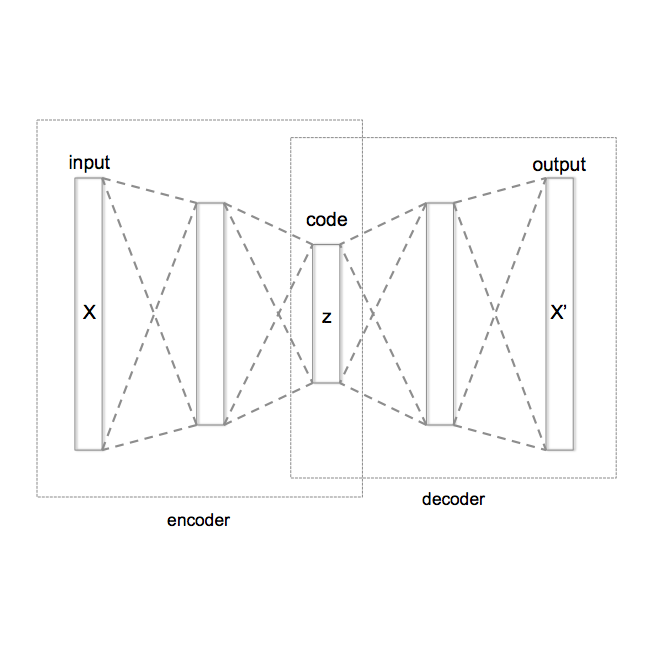

Albeit of crucial interest for both financial practitioners and researchers, market-implied volatility data of European swaptions often exhibit large portions of missing quotes due to illiquidity of the various underlying swaption instruments. In this case, standard stochastic interpolation tools like the common SABR model often cannot be calibrated to observed implied volatility smiles, due to data being only available for the at-the-money quote of the respective underlying swaption. Here, we propose to infer the geometry of the full unknown implied volatility cube by learning stochastic latent representations of implied volatility cubes via variational autoencoders, enabling inference about the missing volatility data conditional on the observed data by an approximate Gibbs sampling approach. Imputed estimates of missing quotes can afterwards be used to fit a standard stochastic volatility model. Since training data for the employed variational autoencoder model is usually sparsely available, we test the robustness of the approach for a model trained on synthetic data on real market quotes and we show that SABR interpolated volatilites calibrated to reconstructed volatility cubes with artificially imputed missing values differ by not much more than two basis points compared to SABR fits calibrated to the complete cube. Moreover, we show how the imputation can be used to successfully set up delta-neutral portfolios for hedging purposes.

翻译:尽管金融从业者和研究人员都非常关心金融业者和研究人员,但市场暗含的欧洲互换的波动数据往往由于各种基本互换工具的流动性不高而出现大量缺失报价。在这种情况下,标准随机互换工具,如共同的SABR模型,往往无法被校准为观察到隐含的波动性微笑,因为只能为各自基本互换的现款报价提供数据。在这里,我们提议通过学习通过变异自动计算器对隐含的波动立方体的随机潜在表示,来推断完全未知的隐含的波动性立方体的几何性。这样可以推断出以所观察到的数据为条件的缺失的波动性数据。之后,对缺失的报价的估算估计数可用于符合标准的随机互换波动性模型。由于所用变异自动互换模型的培训数据通常很少可用,因此我们建议通过在实际市场中进行合成数据培训的模型的稳健性方法进行测试,我们表明,SABR内部对调整的波动性立方体的内在潜在表示,这取决于所观察到的数据,以近似的Gbbs抽样方法,然后再校准再校准再校准的波动基的数值,然后又又以人工校准再校准再校准。