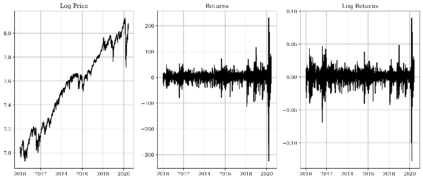

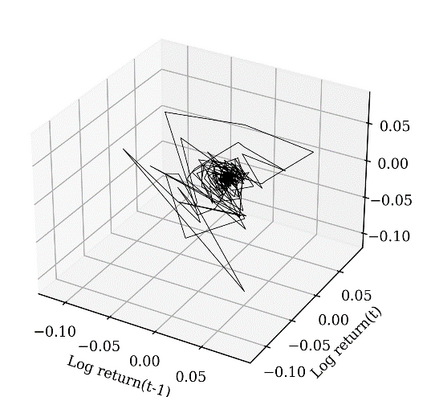

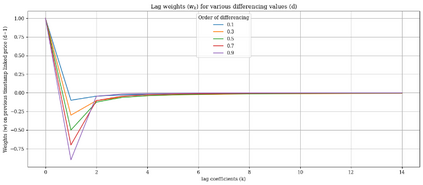

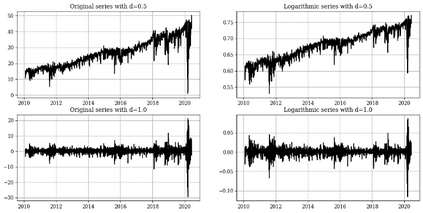

This study introduces a novel forecasting strategy that leverages the power of fractional differencing (FD) to capture both short- and long-term dependencies in time series data. Unlike traditional integer differencing methods, FD preserves memory in series while stabilizing it for modeling purposes. By applying FD to financial data from the SPY index and incorporating sentiment analysis from news reports, this empirical analysis explores the effectiveness of FD in conjunction with binary classification of target variables. Supervised classification algorithms were employed to validate the performance of FD series. The results demonstrate the superiority of FD over integer differencing, as confirmed by Receiver Operating Characteristic/Area Under the Curve (ROCAUC) and Mathews Correlation Coefficient (MCC) evaluations.

翻译:暂无翻译