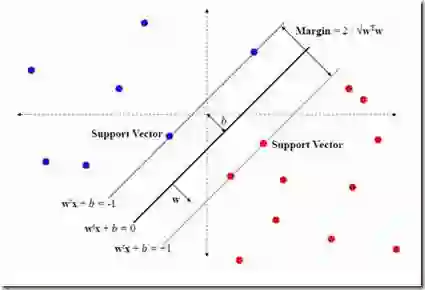

Cryptocurrencies, such as Bitcoin, are one of the most controversial and complex technological innovations in today's financial system. This study aims to forecast the movements of Bitcoin prices at a high degree of accuracy. To this aim, four different Machine Learning (ML) algorithms are applied, namely, the Support Vector Machines (SVM), the Artificial Neural Network (ANN), the Naive Bayes (NB) and the Random Forest (RF) besides the logistic regression (LR) as a benchmark model. In order to test these algorithms, besides existing continuous dataset, discrete dataset was also created and used. For the evaluations of algorithm performances, the F statistic, accuracy statistic, the Mean Absolute Error (MAE), the Root Mean Square Error (RMSE) and the Root Absolute Error (RAE) metrics were used. The t test was used to compare the performances of the SVM, ANN, NB and RF with the performance of the LR. Empirical findings reveal that, while the RF has the highest forecasting performance in the continuous dataset, the NB has the lowest. On the other hand, while the ANN has the highest and the NB the lowest performance in the discrete dataset. Furthermore, the discrete dataset improves the overall forecasting performance in all algorithms (models) estimated.

翻译:Bitcoin等加密是当今金融系统中最有争议和最复杂的技术创新之一,本研究旨在以高度准确性预测比特币价格的变动情况。为此,采用了四种不同的机器学习算法,即支持矢量机(SVM)、人工神经网络(ANN)、Nive Bayes(NB)和随机森林(RF)作为基准模型。为了测试这些算法,除了现有的连续数据集外,还创建和使用离散数据集。对于算法的性能评价,采用了F统计、准确性统计、中度绝对错误(MAE)、根平均值平方错误(RMSE)和根绝对错误(RAE)等四个不同的机器学习算法,即支持矢量机机机机机机机机机机机机机、人工神经网络(ANNNN、NB和RF(RF)作为基准模型;为了测试这些算法,除了现有的连续数据集外,还创建和使用离散数据集。为了评估,RF在连续数据集中预测性能最高,国家数据库(NB)的总体性能水平最低。</s>