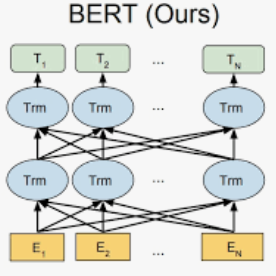

Based on the commentary data of the Shenzhen Stock Index bar on the EastMoney website from January 1, 2018 to December 31, 2019. This paper extracts the embedded investor sentiment by using a deep learning BERT model and investigates the time-varying linkage between investment sentiment, stock market liquidity and volatility using a TVP-VAR model. The results show that the impact of investor sentiment on stock market liquidity and volatility is stronger. Although the inverse effect is relatively small, it is more pronounced with the state of the stock market. In all cases, the response is more pronounced in the short term than in the medium to long term, and the impact is asymmetric, with shocks stronger when the market is in a downward spiral.

翻译:根据2018年1月1日至2019年12月31日东部货币网站上深圳股票指数栏的评注数据,本文件通过采用深思熟虑的BERT模型,总结了投资者的内在情绪,并用TVP-VAR模型调查投资情绪、股票市场流动性和波动之间的时间变化联系。结果显示投资者对股票市场流动性和波动性的影响更大。虽然反效果相对较小,但随着股票市场状况的恶化,这种反应更为明显。 在所有情况下,短期反应比中长期反应更为明显,其影响是不对称的,当市场处于下行螺旋时冲击力更大。