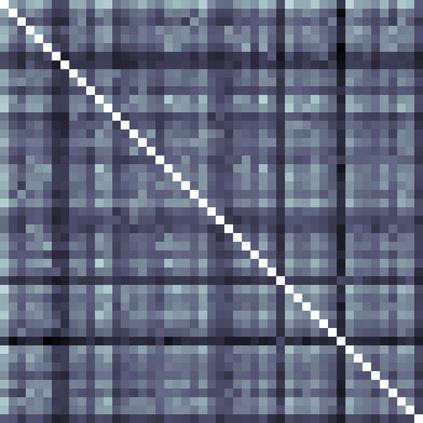

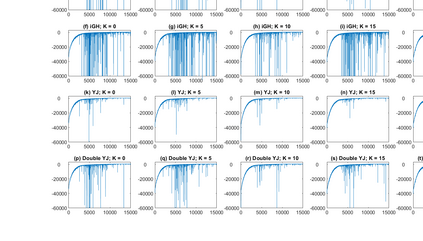

Key to effective generic, or "black-box", variational inference is the selection of an approximation to the target density that balances accuracy and speed. Copula models are promising options, but calibration of the approximation can be slow for some choices. Smith et al. (2020) suggest using tractable and scalable "implicit copula" models that are formed by element-wise transformation of the target parameters. We propose an adjustment to these transformations that make the approximation invariant to the scale and location of the target density. We also show how a sub-class of elliptical copulas have a generative representation that allows easy application of the re-parameterization trick and efficient first order optimization. We demonstrate the estimation methodology using two statistical models as examples. The first is a mixed effects logistic regression, and the second is a regularized correlation matrix. For the latter, standard Markov chain Monte Carlo estimation methods can be slow or difficult to implement, yet our proposed variational approach provides an effective and scalable estimator. We illustrate by estimating a regularized Gaussian copula model for income inequality in U.S. states between 1917 and 2018. An Online Appendix and MATLAB code to implement the method are available as Supplementary Materials.

翻译:有效通用或“黑箱”的钥匙,变式推论是选择接近目标密度的近似值,以平衡准确性和速度。 Copula 模型是很有希望的选择,但近近似校准对于某些选择来说可能是缓慢的。 Smith 等人(2020年)建议使用由目标参数元素转换而形成的可移动和可缩放的“隐性相交”模型。我们建议对这些转换进行调整,使近似值与目标密度的规模和位置不相容。我们还表明,一个小类的椭圆三角形如何具有基因化的表示法,便于应用再校准技巧和高效的第一顺序优化。我们用两种统计模型来展示估算方法,第一种是物流回归的混合效应,第二种是常规化的关联矩阵。对于后者,标准的Markov链 Monte Carlo估算方法可能缓慢或难以实施,然而,我们提议的变异方法提供了有效和可缩的估量法。我们通过估算一个常规化的Gautsian Copulation Capular 模型,用于U.S.