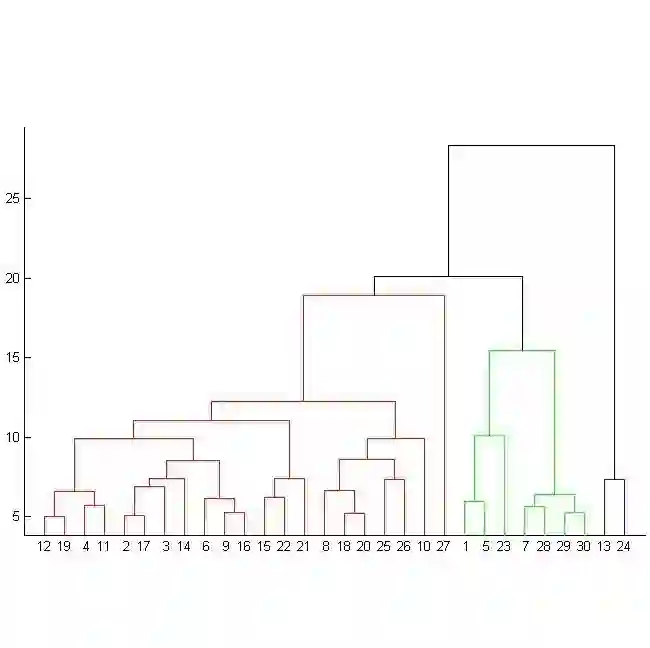

Distance correlation coefficient (DCC) can be used to identify new associations and correlations between multiple variables. The distance correlation coefficient applies to variables of any dimension, can be used to determine smaller sets of variables that provide equivalent information, is zero only when variables are independent, and is capable of detecting nonlinear associations that are undetectable by the classical Pearson correlation coefficient (PCC). Hence, DCC provides more information than the PCC. We analyze numerous pairs of stocks in S\&P500 database with the distance correlation coefficient and provide an overview of stochastic evolution of financial market states based on these correlation measures obtained using agglomerative clustering.

翻译:远程相关系数(DCC)可用于确定多个变量之间的新的关联和关联。远程相关系数适用于任何层面的变量,可用于确定提供同等信息的较小数据集变量,只有在变量独立的情况下,才为零,并且能够检测出无法被古典皮尔逊相关系数(PCC)探测到的非线性关联。因此,DCC比PCC提供更多的信息。我们分析了S ⁇ P500数据库中与远程相关系数的多对股票,并根据利用聚合群获得的这些相关计量,对金融市场国家的变化进行了总体分析。