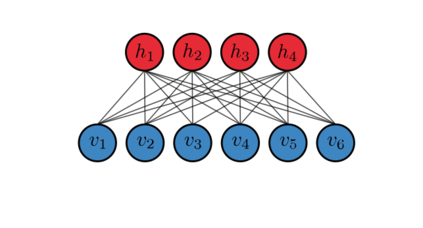

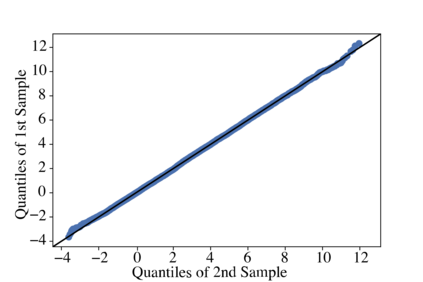

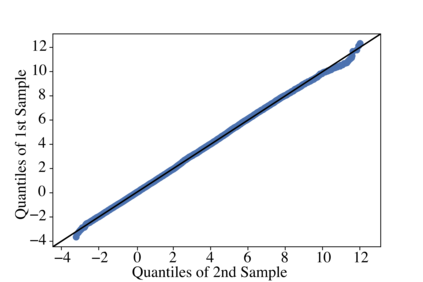

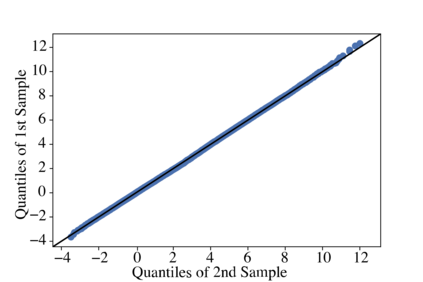

We introduce the notion of Point in Time Economic Scenario Generation (PiT ESG) with a clear mathematical problem formulation to unify and compare economic scenario generation approaches conditional on forward looking market data. Such PiT ESGs should provide quicker and more flexible reactions to sudden economic changes than traditional ESGs calibrated solely to long periods of historical data. We specifically take as economic variable the S&P500 Index with the VIX Index as forward looking market data to compare the nonparametric filtered historical simulation, GARCH model with joint likelihood estimation (parametric), Restricted Boltzmann Machine and the conditional Variational Autoencoder (Generative Networks) for their suitability as PiT ESG. Our evaluation consists of statistical tests for model fit and benchmarking the out of sample forecasting quality with a strategy backtest using model output as stop loss criterion. We find that both Generative Networks outperform the nonparametric and classic parametric model in our tests, but that the CVAE seems to be particularly well suited for our purposes: yielding more robust performance and being computationally lighter.

翻译:我们引入了 " 时间经济情景生成点 " (PiT ESG)的概念,以明确的数学问题公式为基础,统一和比较以前瞻性市场数据为条件的经济情景生成方法。这种PiT ESG应该比仅根据长期历史数据校准的传统 ESGs 更快捷和灵活地对突发经济变化作出反应。我们特别将S & P500指数和VIX指数作为经济变量,作为前瞻性市场数据,以比较非参数过滤历史模拟、GARCH模型和联合概率估计(参数)、限制的Boltzmann机器和有条件的Variational Autoencoder(General Networks),以适合PiT ESG为条件。我们的评估包括模型的统计测试,用模型输出作为停止损失的标准,将抽样预测质量与战略的反测试相匹配。我们发现,两种基因网络都超越了我们测试中的非参数和经典参数模型,但CVAE似乎特别适合我们的目的:产生更稳健的性性表现,计算较轻。