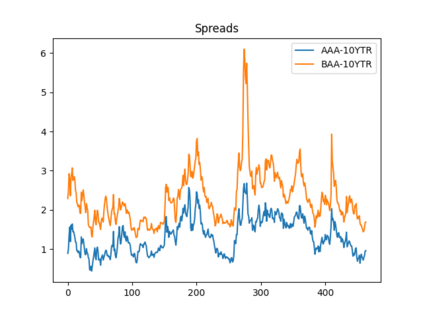

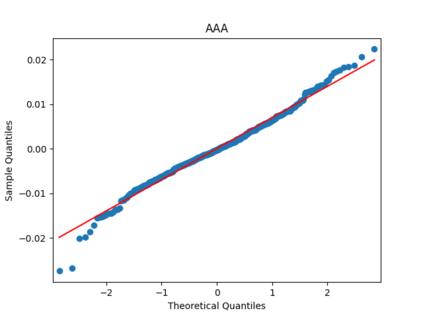

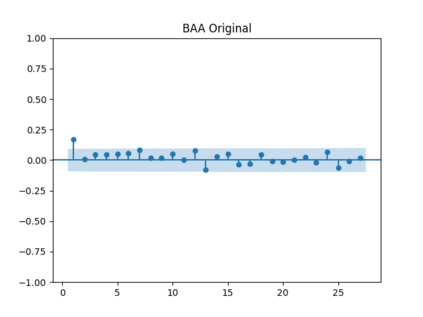

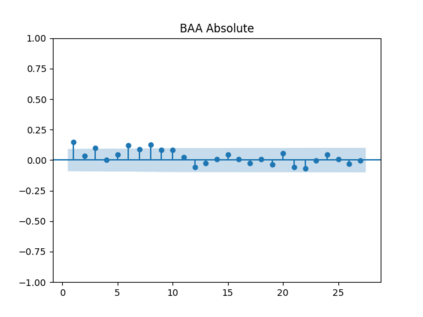

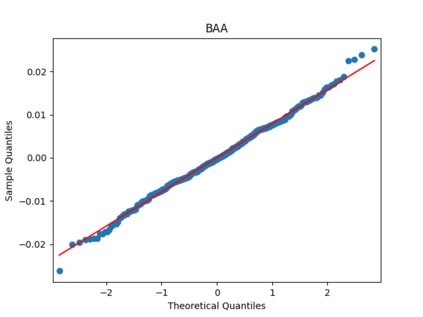

Classic stochastic volatility models assume volatility is unobservable. We use the VIX for consider it observable, and use the Volatility Index: S\&P 500 VIX. This index was designed to measure volatility of S&P 500. We apply it to a different segment: Corporate bond markets. We fit time series models for spreads between corporate and 10-year Treasury bonds. Next, we divide residuals by VIX. Our main idea is such division makes residuals closer to the ideal case of a Gaussian white noise. This is remarkable, since these residuals and VIX come from separate market segments. We also discuss total returns of Bank of America corporate bonds. We conclude with the analysis of long-term behavior of these models.

翻译:暂无翻译

相关内容

ACM/IEEE第23届模型驱动工程语言和系统国际会议,是模型驱动软件和系统工程的首要会议系列,由ACM-SIGSOFT和IEEE-TCSE支持组织。自1998年以来,模型涵盖了建模的各个方面,从语言和方法到工具和应用程序。模特的参加者来自不同的背景,包括研究人员、学者、工程师和工业专业人士。MODELS 2019是一个论坛,参与者可以围绕建模和模型驱动的软件和系统交流前沿研究成果和创新实践经验。今年的版本将为建模社区提供进一步推进建模基础的机会,并在网络物理系统、嵌入式系统、社会技术系统、云计算、大数据、机器学习、安全、开源等新兴领域提出建模的创新应用以及可持续性。

官网链接:http://www.modelsconference.org/

专知会员服务

34+阅读 · 2019年10月18日

专知会员服务

36+阅读 · 2019年10月17日

Arxiv

1+阅读 · 2024年12月18日

Arxiv

1+阅读 · 2024年12月16日

Arxiv

1+阅读 · 2024年12月16日

相关VIP内容

专知会员服务

34+阅读 · 2019年10月18日

专知会员服务

36+阅读 · 2019年10月17日

相关资讯