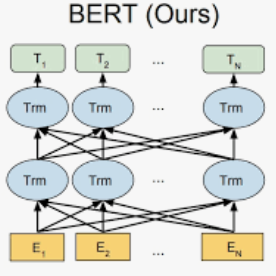

News events can greatly influence equity markets. In this paper, we are interested in predicting the short-term movement of stock prices after financial news events using only the headlines of the news. To achieve this goal, we introduce a new text mining method called Fine-Tuned Contextualized-Embedding Recurrent Neural Network (FT-CE-RNN). Compared with previous approaches which use static vector representations of the news (static embedding), our model uses contextualized vector representations of the headlines (contextualized embeddings) generated from Bidirectional Encoder Representations from Transformers (BERT). Our model obtains the state-of-the-art result on this stock movement prediction task. It shows significant improvement compared with other baseline models, in both accuracy and trading simulations. Through various trading simulations based on millions of headlines from Bloomberg News, we demonstrate the ability of this model in real scenarios.

翻译:新闻事件可以极大地影响股市。 在本文中,我们有兴趣预测金融新闻事件后股票价格的短期变动,只使用新闻的标题。为了实现这一目标,我们引入了一种新的文字开采方法,称为“精密初始背景环境-嵌入式神经网络 ” ( FT-CE-RNN ) 。 与以往使用静态媒介对新闻进行表述(静态嵌入)的方法相比,我们的模型使用了由变压器的双向编码代表生成的头条(通缩嵌入)的根据背景的矢量表达方式。我们的模型获得了这次股票流动预测任务的最新结果。它与其他基线模型相比,在精确度和贸易模拟方面都取得了显著的改进。通过基于布隆伯格新闻数百万条头条的标题进行的各种交易模拟,我们展示了这一模型在真实情景中的能力。