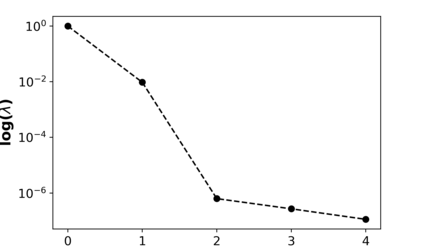

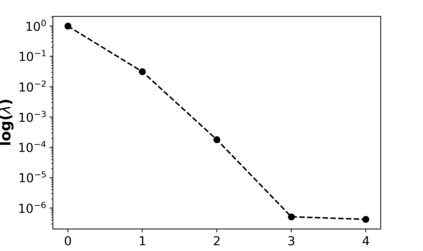

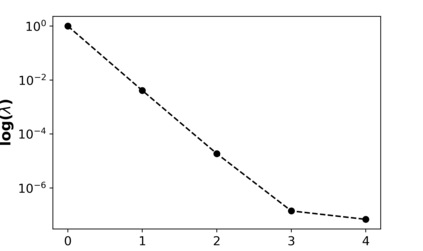

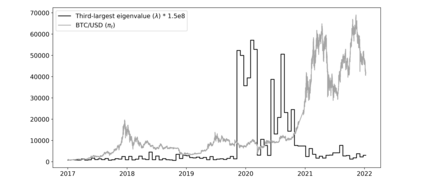

The goals of this paper are twofold: (1) to present a new method that is able to find linear laws governing the time evolution of Markov chains and (2) to apply this method for anomaly detection in Bitcoin prices. To accomplish these goals, first, the linear laws of Markov chains are derived by using the time embedding of their (categorical) autocorrelation function. Then, a binary series is generated from the first difference of Bitcoin exchange rate (against the United States Dollar). Finally, the minimum number of parameters describing the linear laws of this series is identified through stepped time windows. Based on the results, linear laws typically became more complex (containing an additional third parameter that indicates hidden Markov property) in two periods: before the crash of cryptocurrency markets inducted by the COVID-19 pandemic (12 March 2020), and before the record-breaking surge in the price of Bitcoin (Q4 2020 - Q1 2021). In addition, the locally high values of this third parameter are often related to short-term price peaks, which suggests price manipulation.

翻译:本文有两个目标:(1) 提出一种新的方法,能够找到关于Markov链条时间演变的线性法律;(2) 应用这一方法在Bitcoin价格中发现异常现象;为实现这些目标,首先,Markov链条线性法律是利用其(分类的)自动关系功能的时间嵌入而得出的;然后,从Bitcoin汇率的第一个差异(美元对美元)中产生一个二进制系列;最后,描述这一系列线性法律的最低参数数目是通过加速时间窗口确定的;根据结果,线性法律通常在两个时期变得更加复杂(包含额外的第三个参数,表明隐藏的Markov财产):在COVID-19大流行引发的加密货币市场崩溃之前(2020年3月12日),以及在Bitcoin价格破纪录猛涨之前(Q4 2020 - Q1 2021),此外,这第三个参数的当地高值往往与短期价格峰值有关,这表明价格操纵。