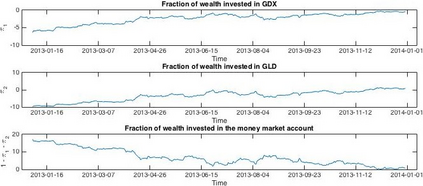

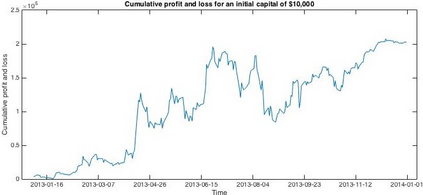

We propose a pairs trading model that incorporates a time-varying volatility of the Constant Elasticity of Variance type. Our approach is based on stochastic control techniques; given a fixed time horizon and a portfolio of two co-integrated assets, we define the trading strategies as the portfolio weights maximizing the expected power utility from terminal wealth. We compute the optimal pairs strategies by using a Finite Difference method. Finally, we illustrate our results by conducting tests on historical market data at daily frequency. The parameters are estimated by the Generalized Method of Moments.

翻译:我们建议一种配对交易模式,其中包括差异类型常量易变性的时差波动性。我们的方法以随机控制技术为基础;考虑到固定的时间跨度和两个共同集成资产组合,我们将贸易战略定义为组合权重,最大限度地发挥终端财富的预期功用。我们通过使用“细差差异”方法计算最佳对子战略。最后,我们通过每天频率对历史市场数据进行测试来说明我们的结果。参数由“通用时数方法”估算。