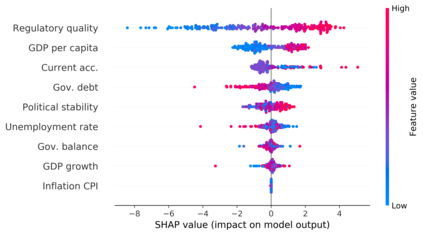

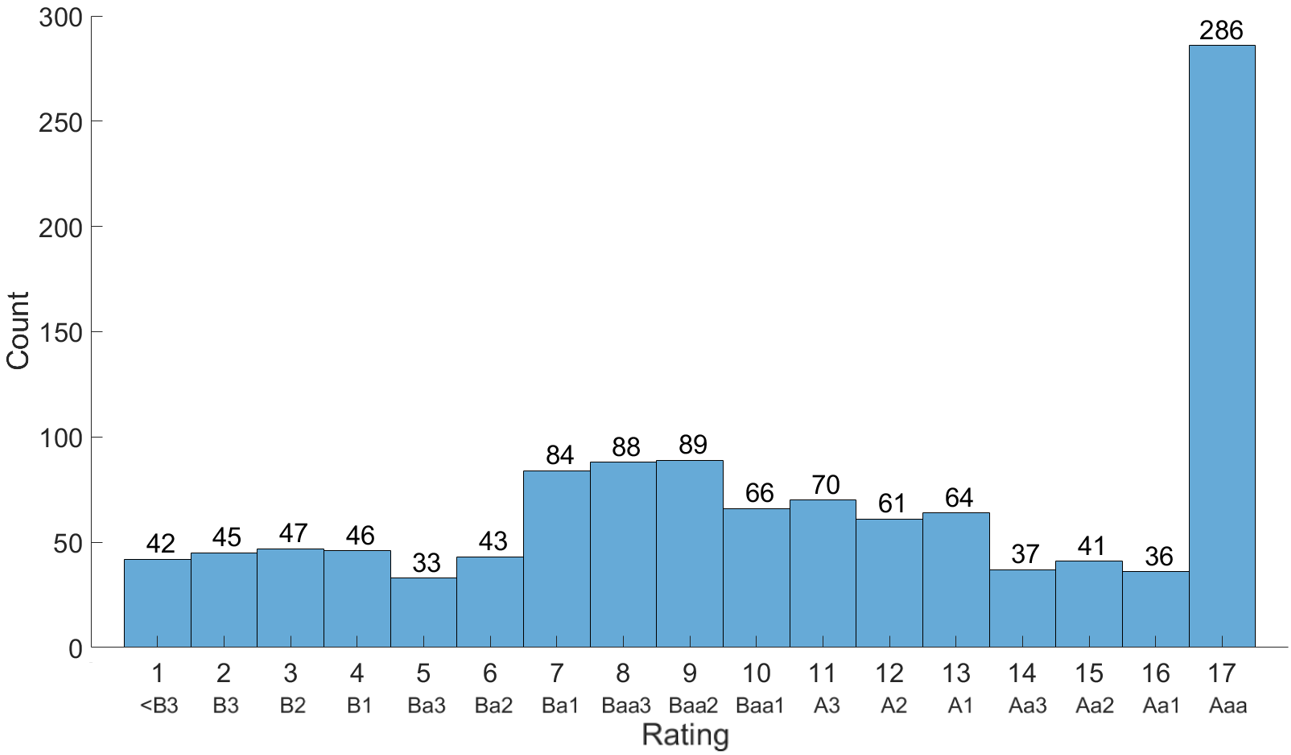

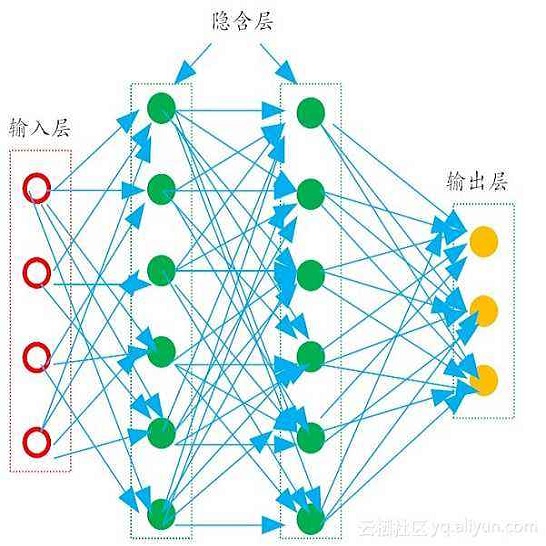

Sovereign credit ratings summarize the creditworthiness of countries. These ratings have a large influence on the economy and the yields at which governments can issue new debt. This paper investigates the use of a Multilayer Perceptron (MLP), Classification and Regression Trees (CART), and an Ordered Logit (OL) model for the prediction of sovereign credit ratings. We show that MLP is best suited for predicting sovereign credit ratings, with an accuracy of 68%, followed by CART (59%) and OL (33%). Investigation of the determining factors shows that roughly the same explanatory variables are important in all models, with regulatory quality, GDP per capita and unemployment rate as common important variables. Consistent with economic theory, a higher regulatory quality and/or GDP per capita are associated with a higher credit rating, while a higher unemployment rate is associated with a lower credit rating.

翻译:主权信用评级总结了各国的信誉。 这些评级对经济和政府发行新债务的收益率有很大影响。 本文调查使用多层受控者(MLP ) 、 分类和递减树(CART ) 和 有序逻辑(OL ) 模型来预测主权信用评级。 我们显示,最低信用评级最适合预测主权信用评级,准确率为68%,其次是CART ( 59%) 和 OL (33% ) 。 对决定因素的调查表明,在所有模型中,基本相同的解释变量都很重要,监管质量、人均GDP和失业率是通用的重要变量。 与经济理论一致,更高的监管质量和(或)人均GDP与更高的信用评级相关联,而更高的失业率与较低的信用评级相关联。