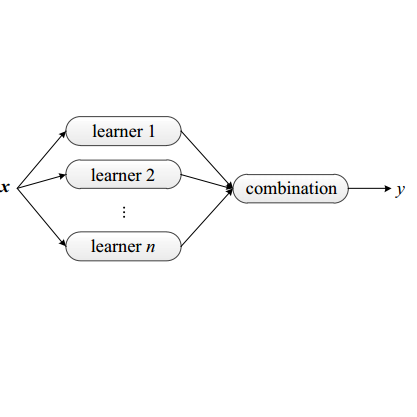

We introduce an ensemble learning method based on Gaussian Process Regression (GPR) for predicting conditional expected stock returns given stock-level and macro-economic information. Our ensemble learning approach significantly reduces the computational complexity inherent in GPR inference and lends itself to general online learning tasks. We conduct an empirical analysis on a large cross-section of US stocks from 1962 to 2016. We find that our method dominates existing machine learning models statistically and economically in terms of out-of-sample $R$-squared and Sharpe ratio of prediction-sorted portfolios. Exploiting the Bayesian nature of GPR, we introduce the mean-variance optimal portfolio with respect to the predictive uncertainty distribution of the expected stock returns. It appeals to an uncertainty averse investor and significantly dominates the equal- and value-weighted prediction-sorted portfolios, which outperform the S&P 500.

翻译:我们采用了基于高斯进程倒退(GPR)的混合学习方法,根据股票水平和宏观经济信息预测有条件的预期股票回报。我们的混合学习方法大大减少了GPR推断所固有的计算复杂性,并有利于一般在线学习任务。我们从1962年至2016年对大量的美国股票进行了经验分析。我们发现,从统计上和经济上看,我们的方法主导了现有机器学习模式,即预测组合的超模值和纯度比率。利用GPR的巴伊西亚性质,我们在预期股票回报的预测不确定性分布方面引入了中值差最佳组合。这引起了不确定性,大大支配了等量和价值加权的预测组合,这些组合超过了S & P 500。