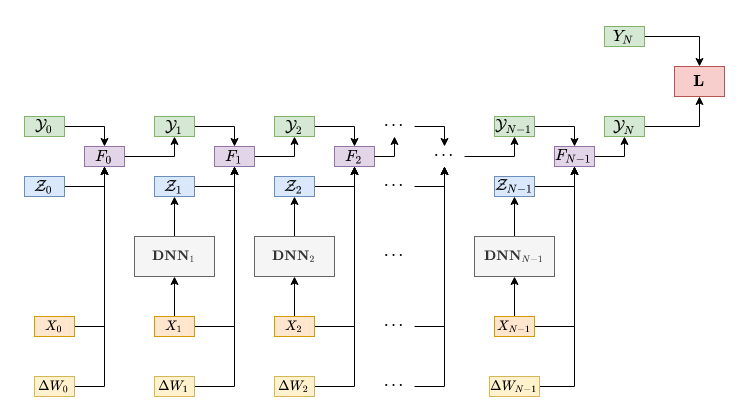

We study deep learning-based schemes for solving high dimensional nonlinear backward stochastic differential equations (BSDEs). First we show how to improve the performances of the proposed scheme in [W. E and J. Han and A. Jentzen, Commun. Math. Stat., 5 (2017), pp.349-380] regarding computational time by using a single neural network architecture instead of the stacked deep neural networks. Furthermore, those schemes can be stuck in poor local minima or diverges, especially for a complex solution structure and longer terminal time. To solve this problem, we investigate to reformulate the problem by including local losses and exploit the Long Short Term Memory (LSTM) networks which are a type of recurrent neural networks (RNN). Finally, in order to study numerical convergence and thus illustrate the improved performances with the proposed methods, we provide numerical results for several 100-dimensional nonlinear BSDEs including nonlinear pricing problems in finance.

翻译:我们研究深层次的基于学习的计划,以解决高维非线性后退蒸气差异方程式(BSDEs)问题。首先,我们展示了如何通过使用单一神经网络结构而不是堆叠的深层神经网络网络来改进计算时间[W.E和J.Han和A.Jentzen,Commun.Matth.Stat., 5 (2017), pp.349-380]中提议的计划绩效。此外,这些计划可能困在贫穷的当地微型或差异中,特别是复杂的解决方案结构和更长的终端时间。为了解决这个问题,我们调查如何重新界定这一问题,包括当地损失,并利用长期短期内存网络,后者是一种经常性的神经网络(RNN)类型。 最后,为了研究数字趋同,从而说明与拟议方法相比的改进绩效,我们为若干100维的非线性BSDE提供了数字结果,包括金融的非线性定价问题。