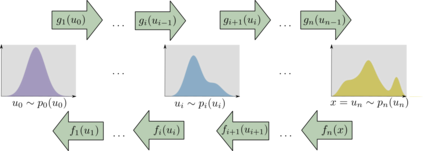

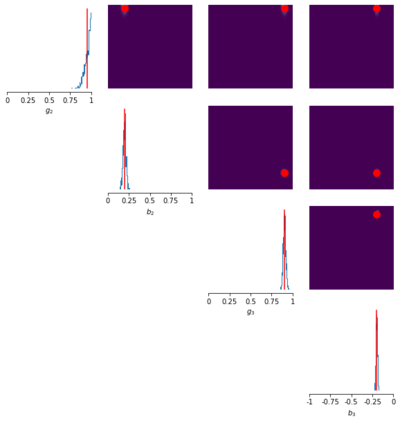

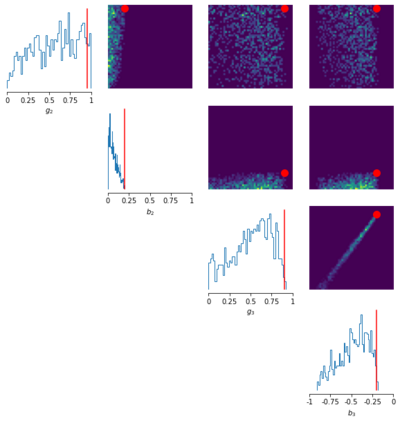

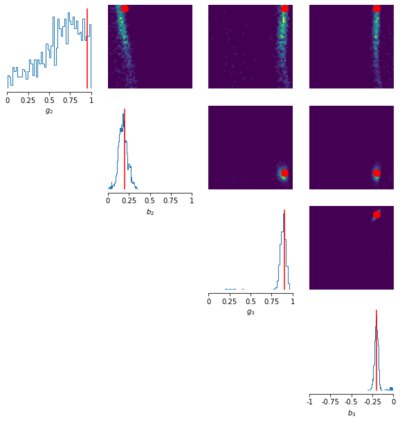

Simulation models, in particular agent-based models, are gaining popularity in economics. The considerable flexibility they offer, as well as their capacity to reproduce a variety of empirically observed behaviours of complex systems, give them broad appeal, and the increasing availability of cheap computing power has made their use feasible. Yet a widespread adoption in real-world modelling and decision-making scenarios has been hindered by the difficulty of performing parameter estimation for such models. In general, simulation models lack a tractable likelihood function, which precludes a straightforward application of standard statistical inference techniques. Several recent works have sought to address this problem through the application of likelihood-free inference techniques, in which parameter estimates are determined by performing some form of comparison between the observed data and simulation output. However, these approaches are (a) founded on restrictive assumptions, and/or (b) typically require many hundreds of thousands of simulations. These qualities make them unsuitable for large-scale simulations in economics and can cast doubt on the validity of these inference methods in such scenarios. In this paper, we investigate the efficacy of two classes of black-box approximate Bayesian inference methods that have recently drawn significant attention within the probabilistic machine learning community: neural posterior estimation and neural density ratio estimation. We present benchmarking experiments in which we demonstrate that neural network based black-box methods provide state of the art parameter inference for economic simulation models, and crucially are compatible with generic multivariate time-series data. In addition, we suggest appropriate assessment criteria for future benchmarking of approximate Bayesian inference procedures for economic simulation models.

翻译:模拟模型,特别是以代理商为基础的模拟模型,在经济学中越来越受欢迎。它们所提供的相当灵活,以及它们复制复杂系统各种经经验观察到的行为的能力,使这些系统具有广泛的吸引力,而且越来越容易获得廉价的计算能力,使得使用这些模型成为可行。然而,在现实世界模型和决策假设中广泛采用这些模型却由于难以为这些模型进行参数估计而受阻。一般而言,模拟模型缺乏可移植的可能性功能,无法直接应用标准统计推断技术。最近的一些工作设法通过应用无概率推断技术来解决这一问题,在这种技术中,通过对所观测的数据和模拟产出进行某种形式的比较来确定参数估计。然而,这些方法(a)基于限制性假设,和/或(b)通常需要数十万种模拟。这些特性使得这些模型不适合在经济学中进行大规模模拟,并可能使人怀疑此类假设中这些推断方法的正确性。在本文件中,我们调查了两种黑箱比亚近基度推断值的精确度比值比率,通过对所观测的数据进行某种形式的比较比值比值性模型的精确度评估。我们最近在社区进行了精确的模型的精确的精确度估算,从而显示了我们所测测测测测测测测测的网络的比。