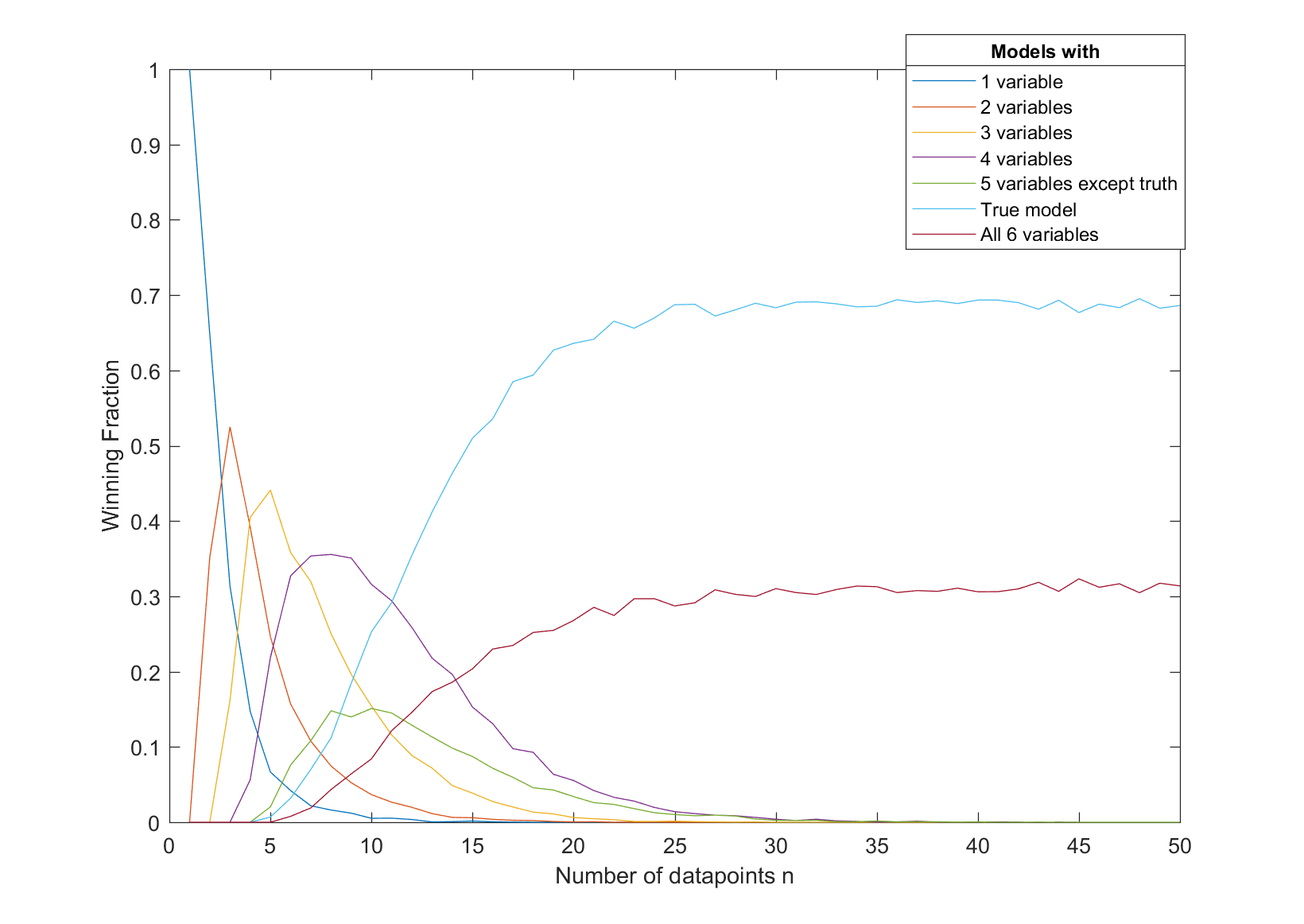

Agents compete to acquire an asset whose value depends on how well they can predict an unknown variable. Agents are Bayesian, observe identical data, but have different models: they use different subsets of explanatory variables to make their predictions. The winning model crucially depends on the sample size. With small samples, we present a number of results suggesting it is an agent using a low-dimensional model, in the sense of using a smaller number of variables relative to the true data generating process. With large samples, we show that it is generally an agent with a high-dimensional model, possibly including irrelevant variables, but never excluding relevant ones.

翻译:代理商竞相获取资产,资产的价值取决于他们能预测出未知变量的程度。代理商是贝叶西亚人,观察相同的数据,但有不同的模型:他们使用不同的解释变量子集作出预测。获胜模型关键取决于样本大小。我们用少量样本提出一些结果,表明它是一个使用低维模型的代理商,与真正的数据生成过程相比,它使用较少数量的变量。用大样本,我们显示它通常是具有高维模型的代理商,可能包括无关的变量,但绝不排除相关的变量。