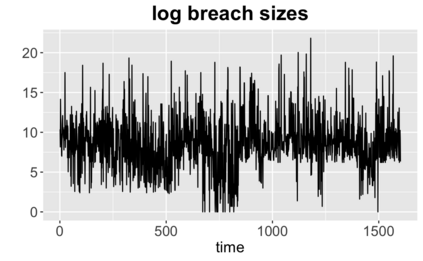

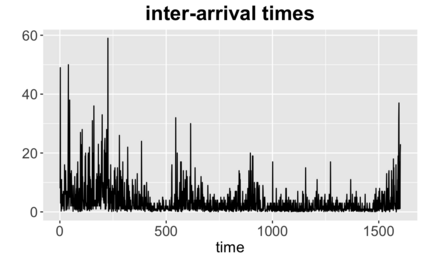

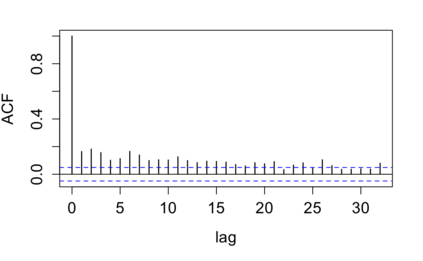

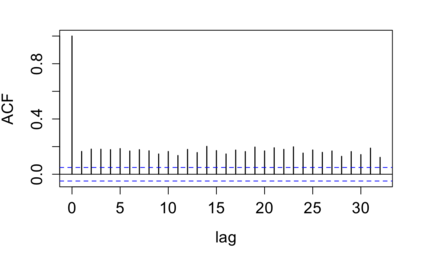

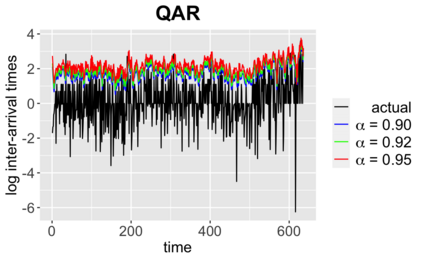

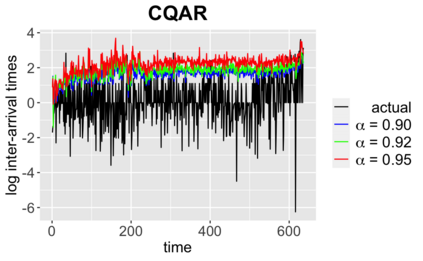

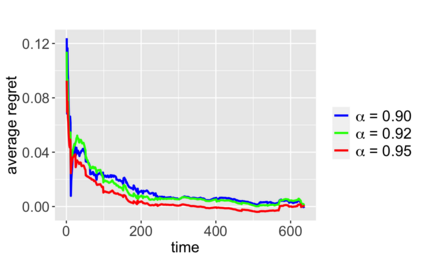

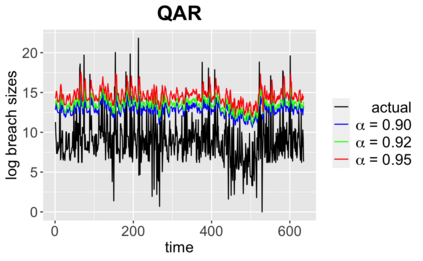

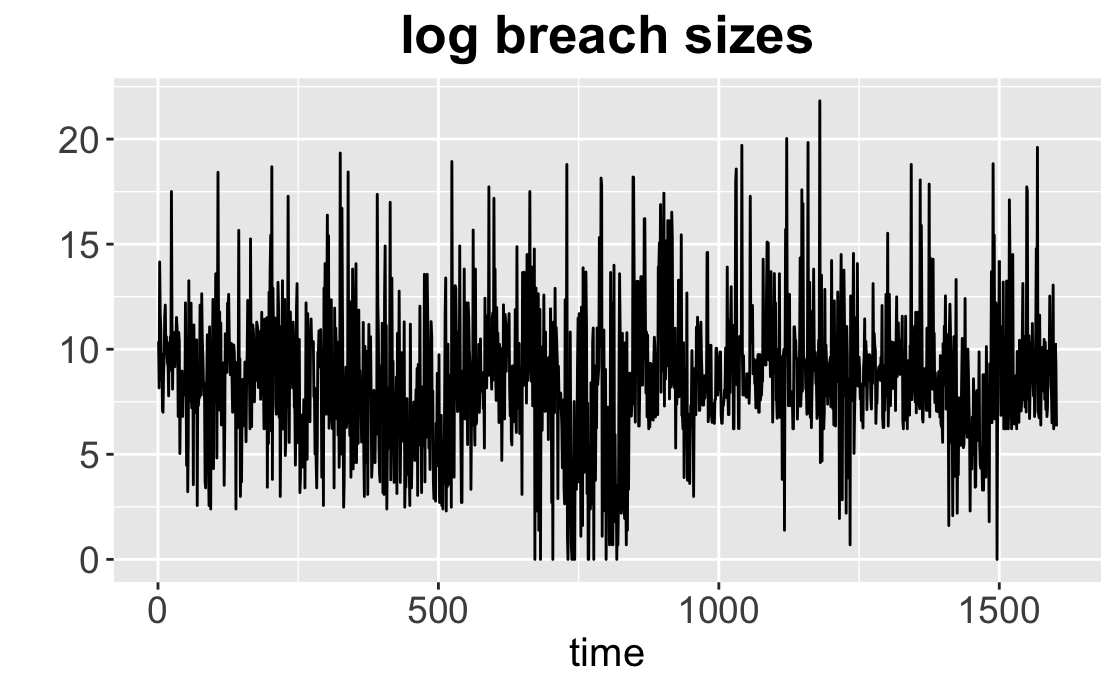

The increasing value of data held in enterprises makes it an attractive target to attackers. The increasing likelihood and impact of a cyber attack have highlighted the importance of effective cyber risk estimation. We propose two methods for modelling Value-at-Risk (VaR) which can be used for any time-series data. The first approach is based on Quantile Autoregression (QAR), which can estimate VaR for different quantiles, i.e. confidence levels. The second method, we term Competitive Quantile Autoregression (CQAR), dynamically re-estimates cyber risk as soon as new data becomes available. This method provides a theoretical guarantee that it asymptotically performs as well as any QAR at any time point in the future. We show that these methods can predict the size and inter-arrival time of cyber hacking breaches by running coverage tests. The proposed approaches allow to model a separate stochastic process for each significance level and therefore provide more flexibility compared to previously proposed techniques. We provide a fully reproducible code used for conducting the experiments.

翻译:企业中掌握的数据价值不断提高,使得它成为攻击者的吸引力目标。网络攻击的可能性和影响日益增加,突出了有效网络风险估计的重要性。我们提出了两种方法,用于制作可用于任何时间序列数据的 " 风险值 " (VaR)模型,第一种方法基于 " 量子自动递减 " (QAR),该方法可以估计不同量的VaR,即信任度。第二种方法,我们称为 " 竞争性量子自动递减(CQAR) " (CQAR),即一旦获得新的数据,即动态地重新估计网络风险。这个方法提供了一种理论保证,即该方法在任何时间点上都可同时运行以及任何QAR(QAR),我们表明这些方法可以通过进行覆盖测试来预测网络黑破碎的大小和间隔时间。拟议方法允许为每个重要级分别设计一个抽查程序,从而与先前提出的技术相比,具有更大的灵活性。我们提供了用于进行实验的完全重复的代码。