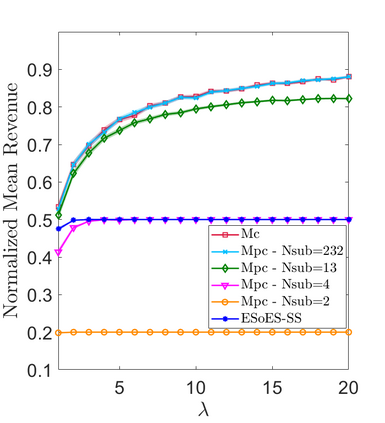

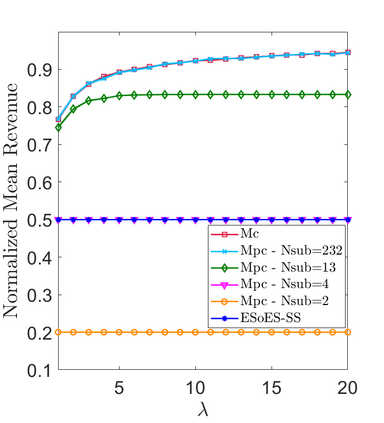

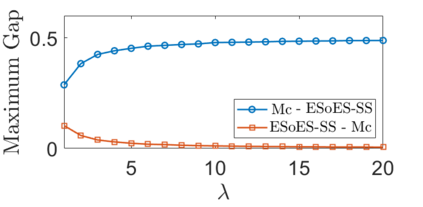

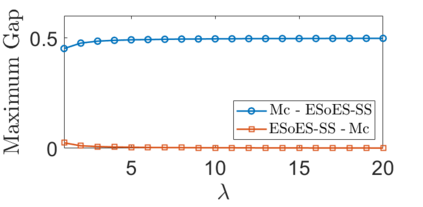

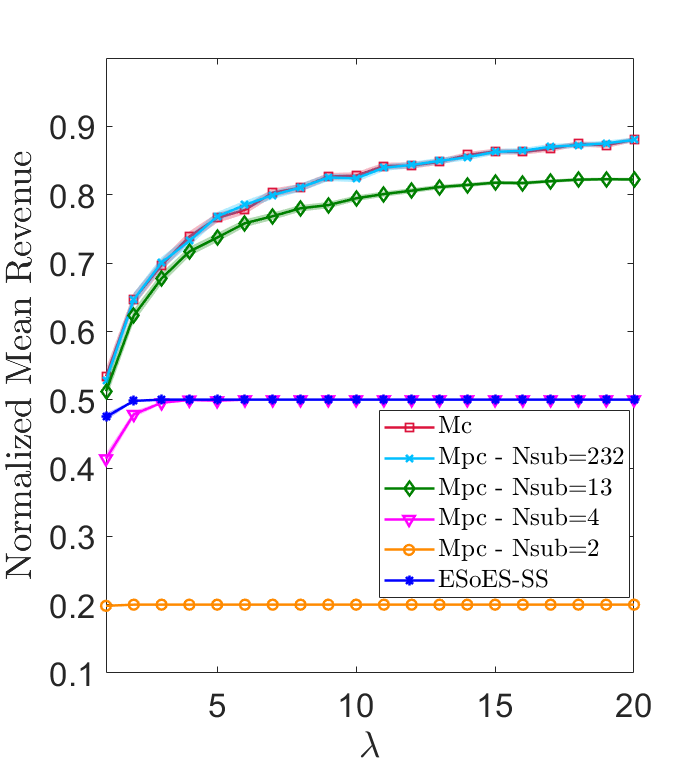

We study the problem of designing posted-price mechanisms in order to sell a single unit of a single item within a finite period of time. Motivated by real-world problems, such as, e.g., long-term rental of rooms and apartments, we assume that customers arrive online according to a Poisson process, and their valuations are drawn from an unknown distribution and discounted over time. We evaluate our mechanisms in terms of competitive ratio, measuring the worst-case ratio between their revenue and that of an optimal mechanism that knows the distribution of valuations. First, we focus on the identical valuation setting, where all the customers value the item for the same amount. In this setting, we provide a mechanism M_c that achieves the best possible competitive ratio, discussing its dependency on the parameters in the case of linear discount. Then, we switch to the random valuation setting. We show that, if we restrict the attention to distributions of valuations with a monotone hazard rate, then the competitive ratio of M_c is lower bounded by a strictly positive constant that does not depend on the distribution. Moreover, we provide another mechanism, called M_pc, which is defined by a piecewise constant pricing strategy and reaches performances comparable to those obtained with M_c. This mechanism is useful when the seller cannot change the posted price too often. Finally, we empirically evaluate the performances of our mechanisms in a number of experimental settings.

翻译:我们研究设计上市价格机制的问题,以在一定时间内出售单一物品的单一单位单位。受长期租赁房间和公寓等现实世界问题的影响,我们假设客户根据Poisson程序上网,而他们的估值是从一个未知的分配和时间折扣中得出的。我们从竞争比率的角度来评估我们的机制,衡量其收入与了解估值分配情况的最佳机制之间的最坏比例。首先,我们侧重于相同的估值设置,所有客户都以相同数额估价该物品。在这个设置中,我们提供了一个M_c机制,实现尽可能最佳的竞争比率,讨论其对线性折扣参数的依赖。然后,我们转向随机估值设置。我们表明,如果我们把注意力限制在使用单一风险率的估值分配上,那么M_c的竞争性比率就更低了,而这种竞争性比率则不取决于分配情况。此外,我们提供了另一个机制,称为M_c机制,即实现最佳竞争比率,讨论其对线性折扣参数的依赖性参数。然后,我们用一个不变的实验性定价机制来界定了我们所获取的数值的数值。我们常常以固定的货币定价为标准。我们用一个固定的货币确定。