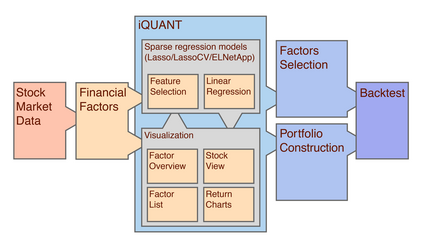

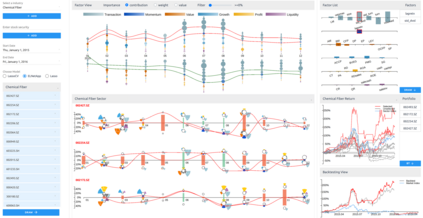

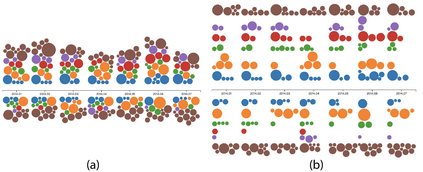

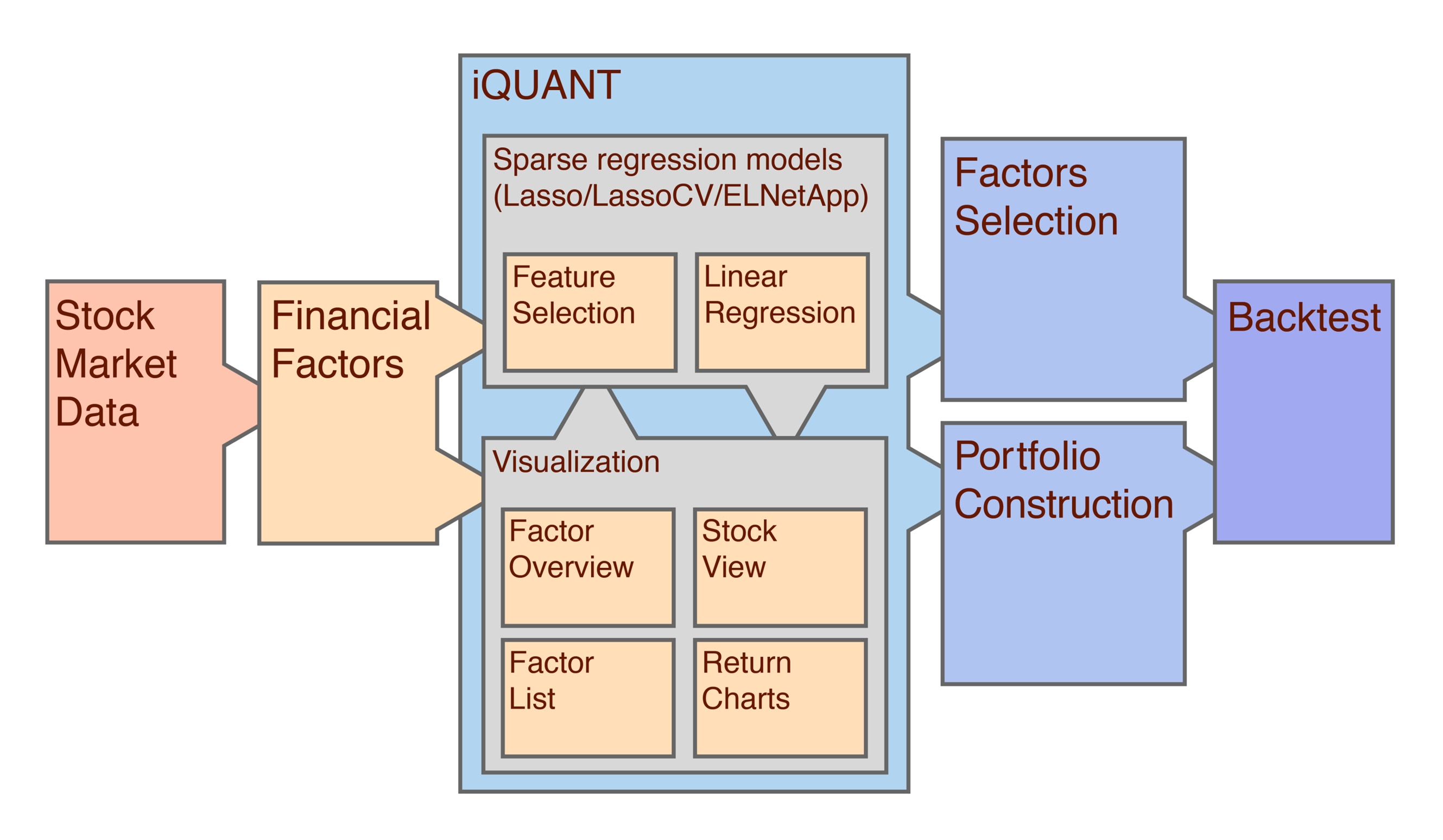

The model-based investing using financial factors is evolving as a principal method for quantitative investment. The main challenge lies in the selection of effective factors towards excess market returns. Existing approaches, either hand-picking factors or applying feature selection algorithms, do not orchestrate both human knowledge and computational power. This paper presents iQUANT, an interactive quantitative investment system that assists equity traders to quickly spot promising financial factors from initial recommendations suggested by algorithmic models, and conduct a joint refinement of factors and stocks for investment portfolio composition. We work closely with professional traders to assemble empirical characteristics of "good" factors and propose effective visualization designs to illustrate the collective performance of financial factors, stock portfolios, and their interactions. We evaluate iQUANT through a formal user study, two case studies, and expert interviews, using a real stock market dataset consisting of 3000 stocks times 6000 days times 56 factors.

翻译:使用金融因素的基于模型的投资正在演变,成为量化投资的主要方法,主要挑战在于选择实现超额市场回报的有效因素; 现有办法,无论是手工选择因素还是应用地物选择算法,都不协调人类知识和计算能力; 本文介绍了iQUANT,这是一个互动的量化投资系统,它帮助股权交易商从算法模型提出的初步建议中迅速发现有希望的金融因素,并联合完善投资组合构成的各种因素和股票; 我们与专业贸易商密切合作,收集“良好”因素的经验特征,并提出有效的可视化设计,以说明金融因素、股票组合及其相互作用的集体表现; 我们通过正式用户研究、两个案例研究和专家访谈,利用由3000个股位乘以6000天乘以56因素组成的实际股票市场数据集,对iQUANT进行评估。