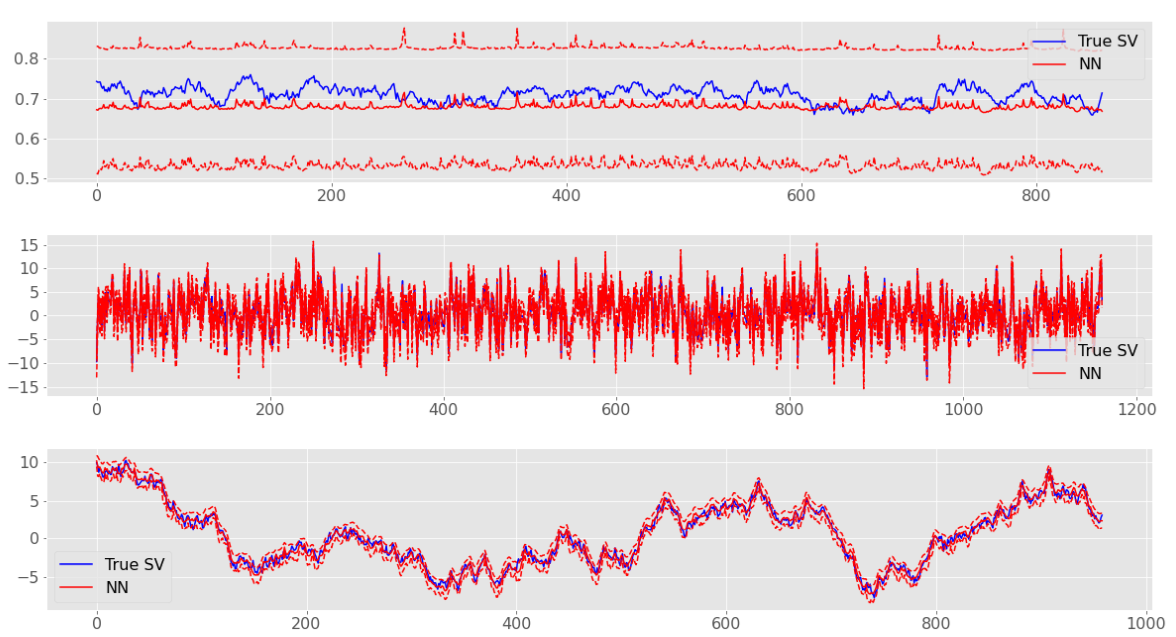

This paper presents a fast algorithm for estimating hidden states of Bayesian state space models. The algorithm is a variation of amortized simulation-based inference algorithms, where a large number of artificial datasets are generated at the first stage, and then a flexible model is trained to predict the variables of interest. In contrast to those proposed earlier, the procedure described in this paper makes it possible to train estimators for hidden states by concentrating only on certain characteristics of the marginal posterior distributions and introducing inductive bias. Illustrations using the examples of the stochastic volatility model, nonlinear dynamic stochastic general equilibrium model, and seasonal adjustment procedure with breaks in seasonality show that the algorithm has sufficient accuracy for practical use. Moreover, after pretraining, which takes several hours, finding the posterior distribution for any dataset takes from hundredths to tenths of a second.

翻译:本文提供了一种快速算法,用于估算巴伊西亚州空间模型的隐蔽状态。算法是分解模拟推断算法的变异,在第一阶段生成了大量人工数据集,然后对一个灵活模型进行了培训,以预测感兴趣的变量。与先前提出的模型不同,本文件描述的程序使得有可能对隐蔽状态的估算师进行培训,仅侧重于边际后部分布的某些特征,并引入感应偏差。 说明使用了随机波动模型、非线性动态随机随机一般平衡模型和季节性间断的季节性调整程序等实例,表明算法具有足够的准确性,可以实际使用。此外,在经过几个小时的预修后,找到任何数据集的后部分布从千分之十到秒十分十分之一不等。