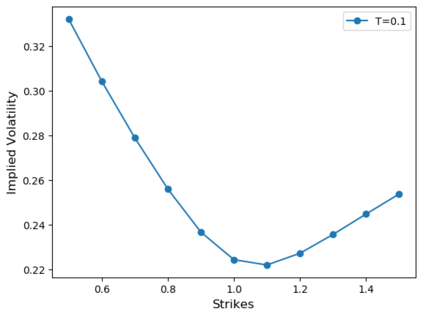

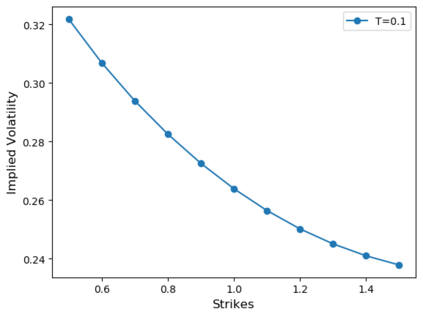

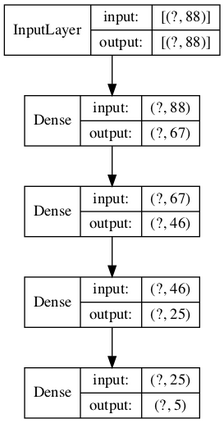

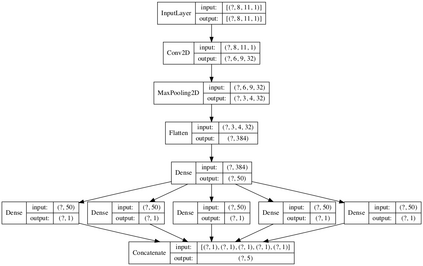

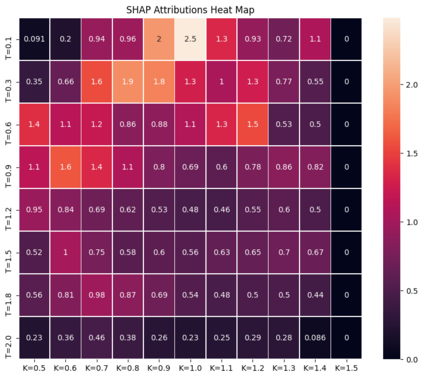

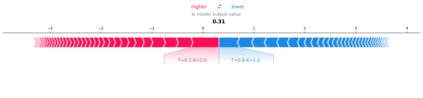

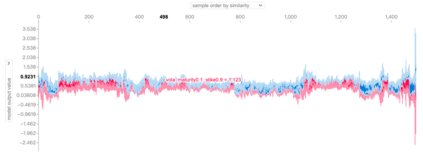

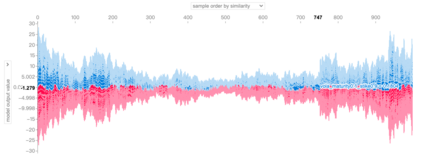

Deep learning is a powerful tool whose applications in quantitative finance are growing every day. Yet, artificial neural networks behave as black boxes and this hinders validation and accountability processes. Being able to interpret the inner functioning and the input-output relationship of these networks has become key for the acceptance of such tools. In this paper we focus on the calibration process of a stochastic volatility model, a subject recently tackled by deep learning algorithms. We analyze the Heston model in particular, as this model's properties are well known, resulting in an ideal benchmark case. We investigate the capability of local strategies and global strategies coming from cooperative game theory to explain the trained neural networks, and we find that global strategies such as Shapley values can be effectively used in practice. Our analysis also highlights that Shapley values may help choose the network architecture, as we find that fully-connected neural networks perform better than convolutional neural networks in predicting and interpreting the Heston model prices to parameters relationship.

翻译:深层学习是一个强大的工具,其应用在量化金融方面每天都在增长。然而,人工神经网络作为黑盒行为,这阻碍了验证和问责进程。能够解释这些网络的内部功能和输入-输出关系已成为接受这些工具的关键。在本文中,我们侧重于随机波动模型的校准过程,这是最近由深层学习算法处理的一个主题。我们特别分析赫斯顿模型,因为该模型的特性众所周知,因此产生了一个理想的基准案例。我们调查了当地战略和全球战略的能力,这些战略和全球战略来自合作游戏理论,以解释受过训练的神经网络,我们发现Shapley值等全球战略可以在实践中得到有效利用。我们的分析还突出表明,Shapley值可能有助于选择网络结构,因为我们发现,完全连接的神经网络在预测和解释赫斯顿模型价格与参数关系方面比革命神经网络表现更好。