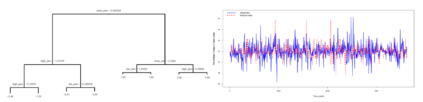

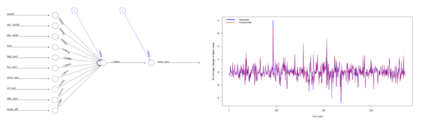

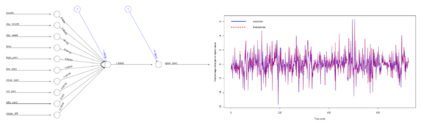

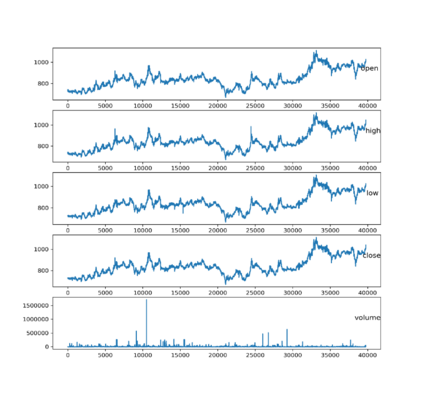

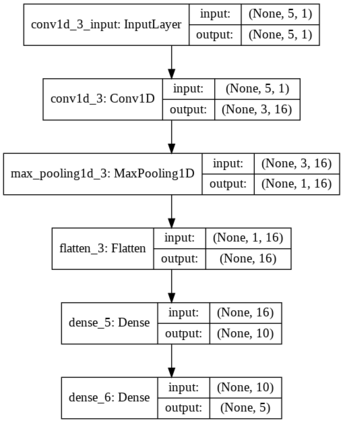

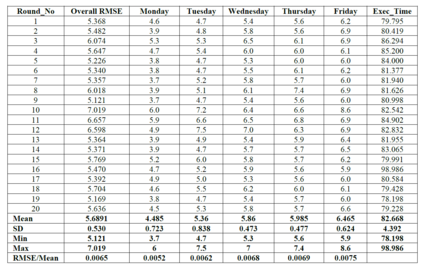

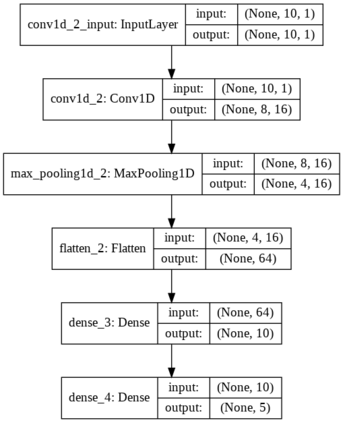

Prediction of future movement of stock prices has always been a challenging task for the researchers. While the advocates of the efficient market hypothesis (EMH) believe that it is impossible to design any predictive framework that can accurately predict the movement of stock prices, there are seminal work in the literature that have clearly demonstrated that the seemingly random movement patterns in the time series of a stock price can be predicted with a high level of accuracy. Design of such predictive models requires choice of appropriate variables, right transformation methods of the variables, and tuning of the parameters of the models. In this work, we present a very robust and accurate framework of stock price prediction that consists of an agglomeration of statistical, machine learning and deep learning models. We use the daily stock price data, collected at five minutes interval of time, of a very well known company that is listed in the National Stock Exchange (NSE) of India. The granular data is aggregated into three slots in a day, and the aggregated data is used for building and training the forecasting models. We contend that the agglomerative approach of model building that uses a combination of statistical, machine learning, and deep learning approaches, can very effectively learn from the volatile and random movement patterns in a stock price data. We build eight classification and eight regression models based on statistical and machine learning approaches. In addition to these models, a deep learning regression model using a long-and-short-term memory (LSTM) network is also built. Extensive results have been presented on the performance of these models, and the results are critically analyzed.

翻译:预测未来股票价格变动的预测一直是研究人员的一项艰巨任务。虽然高效率市场假设(EMH)的倡导者认为,不可能设计任何能够准确预测股票价格变动的预测框架,但文献中的一些开创性工作清楚地表明,股票价格时间序列中似乎随机的变动模式可以高准确度预测。这种预测模型的设计要求选择适当的变量,变量的正确转换方法,以及调整模型参数。在这项工作中,我们提出了一个非常有力和准确的股票价格预测框架,其中包括统计、机器学习和深层学习模型的集合。我们利用在五分钟的间隔内收集的、在印度国家股票交易所(NSE)上市的一家非常知名公司的每日股票价格数据。颗粒数据每天被汇总成三个档次,而汇总数据模型被用于建立和培训预测模型。我们发现,模型建设的聚合方法包括统计模型、机器学习、机器学习和深层学习模型模型。我们从统计模型的8个周期性能到模型的演变,可以有效地学习这些模型。我们从统计、机器学习和深度的8个周期性分析方法。我们从这些统计模型学习到模型的周期性分析方法。