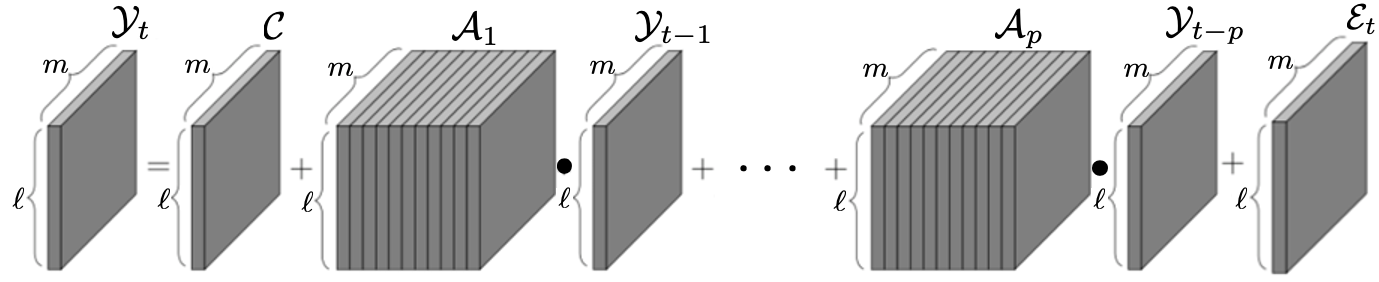

In the era of big data, there is an increasing demand for new methods for analyzing and forecasting 2-dimensional data. The current research aims to accomplish these goals through the combination of time-series modeling and multilinear algebraic systems. We expand previous autoregressive techniques to forecast multilinear data, aptly named the L-Transform Tensor autoregressive (L-TAR for short). Tensor decompositions and multilinear tensor products have allowed for this approach to be a feasible method of forecasting. We achieve statistical independence between the columns of the observations through invertible discrete linear transforms, enabling a divide and conquer approach. We present an experimental validation of the proposed methods on datasets containing image collections, video sequences, sea surface temperature measurements, stock prices, and networks.

翻译:在海量数据时代,对分析和预测二维数据的新方法的需求日益增加。当前研究的目标是通过时间序列模型和多线性代数系统相结合来实现这些目标。我们将以前的自动递减技术扩大到预测多线性数据,适当命名为L-Transfor Tansor自动递减(短称L-TAR),电离分解和多线性高压产品使得这一方法成为可行的预测方法。我们通过不可逆的离散线线性变换实现观测各列之间的统计独立,从而形成分裂和征服方法。我们试验性地验证了包含图像采集、视频序列、海面温度测量、股票价格和网络的数据集的拟议方法。