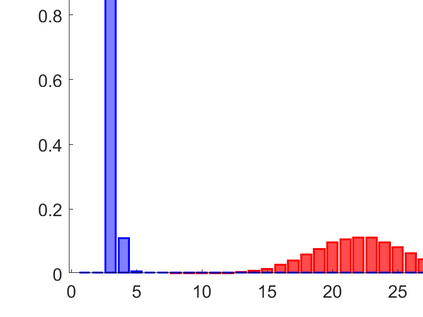

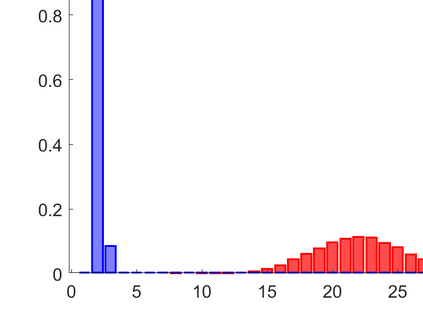

This paper introduces a new model for panel data with Markov-switching GARCH effects. The model incorporates a series-specific hidden Markov chain process that drives the GARCH parameters. To cope with the high-dimensionality of the parameter space, the paper exploits the cross-sectional clustering of the series by first assuming a soft parameter pooling through a hierarchical prior distribution with two-step procedure, and then introducing clustering effects in the parameter space through a nonparametric prior distribution. The model and the proposed inference are evaluated through a simulation experiment. The results suggest that the inference is able to recover the true value of the parameters and the number of groups in each regime. An empirical application to 78 assets of the SP\&100 index from $6^{th}$ January 2000 to $3^{rd}$ October 2020 is also carried out by using a two-regime Markov switching GARCH model. The findings shows the presence of 2 and 3 clusters among the constituents in the first and second regime, respectively.

翻译:本文介绍了关于Markov- switching GARCH效应的面板数据的新模型。 该模型包含一系列特定隐藏的Markov链过程,驱动 GARCH 参数参数。 为了应对参数空间的高度维度, 本文利用了该系列的跨部门组合, 首先假设通过分级前分级分级程序集中一个软参数, 然后通过分级前两步程序在参数空间中引入组合效应。 该模型和拟议的推论通过模拟实验进行评估。 结果表明, 推论能够恢复参数的真实值和每个系统中的组数。 2000年1月6日到2020年10月3日之间,SP ⁇ 100指数的78个资产的经验应用也是通过使用两根基米·马尔科夫转换 GRCH 模型进行的。 研究结果显示,第一和第二系统分别存在2个和3个成分组。