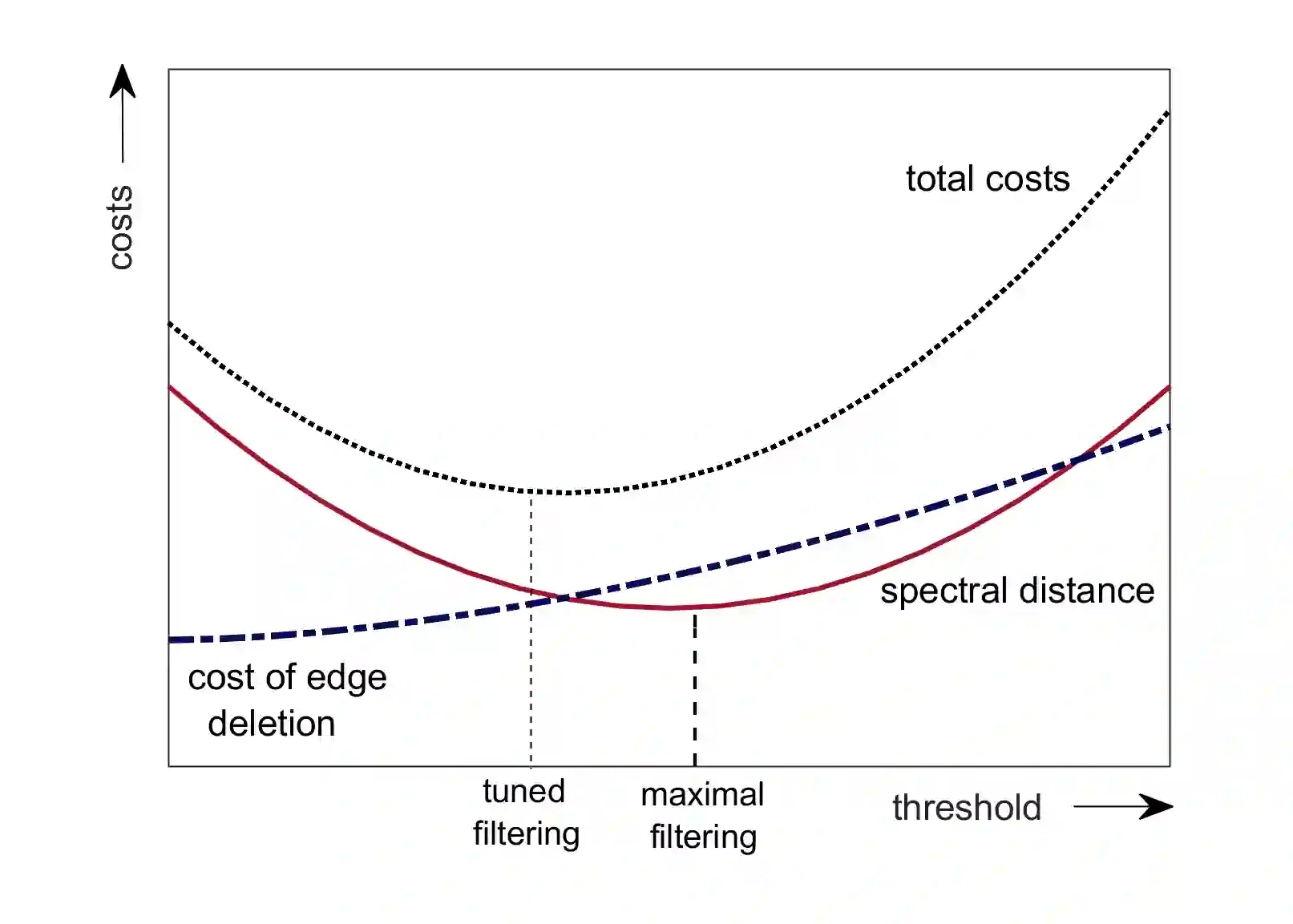

Network filtering is an important form of dimension reduction to isolate the core constituents of large and interconnected complex systems. We introduce a new technique to filter large dimensional networks arising out of dynamical behavior of the constituent nodes, exploiting their spectral properties. As opposed to the well known network filters that rely on preserving key topological properties of the realized network, our method treats the spectrum as the fundamental object and preserves spectral properties. Applying asymptotic theory for high dimensional data for the filter, we show that it can be tuned to interpolate between zero filtering to maximal filtering that induces sparsity and consistency while having the least spectral distance from a linear shrinkage estimator. We apply our proposed filter to covariance networks constructed from financial data, to extract the key subnetwork embedded in the full sample network.

翻译:网络过滤是一种重要的维度递减形式, 以隔离大型和相互关联的复杂系统的核心成分。 我们引入了一种新技术, 过滤由组成节点动态行为产生的大型维网络, 利用它们的光谱特性。 与依靠保存已实现网络的关键地形特性的众所周知的网络过滤器相反, 我们的方法将频谱作为基本对象处理, 并保存光谱特性。 将高维数据应用于无空间理论, 用于过滤器, 我们显示它可以被调换到从零过滤到最大过滤器之间的间隙, 最大过滤器能产生宽度和一致性, 同时从线性缩缩缩缩缩缩缩缩缩缩缩缩缩略图中保持最小的光谱距离。 我们用我们提议的过滤器来利用从财务数据中构建的共变网络, 提取完全样本网络中嵌入的关键子网络。