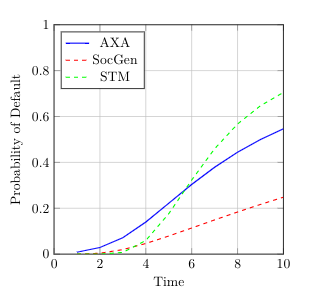

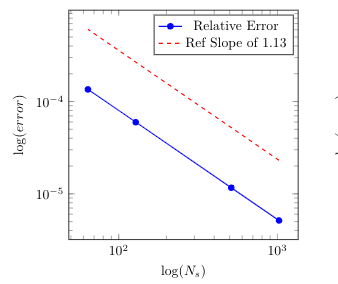

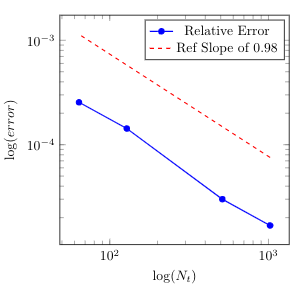

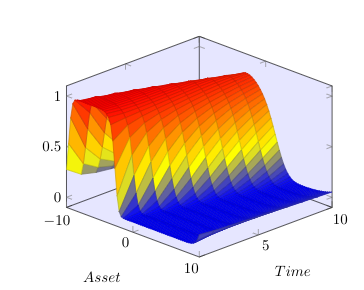

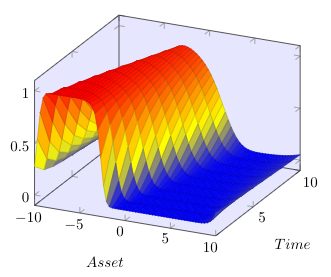

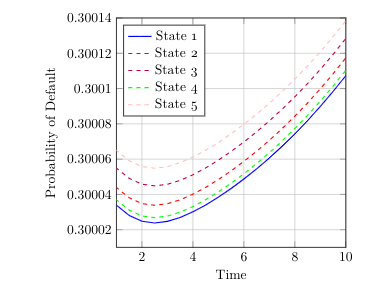

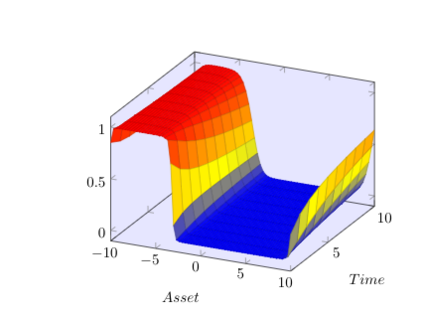

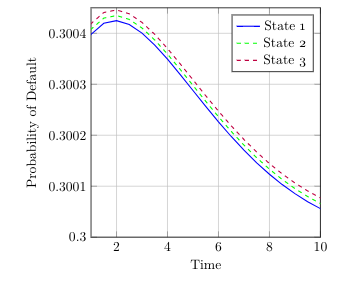

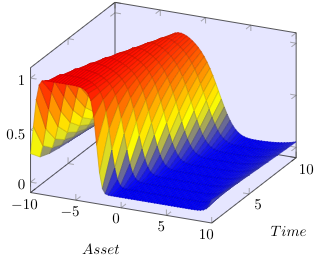

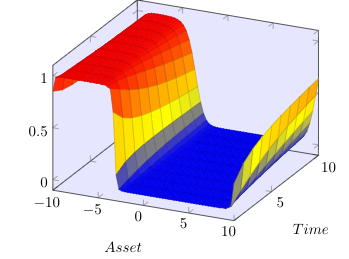

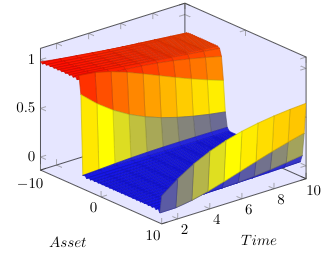

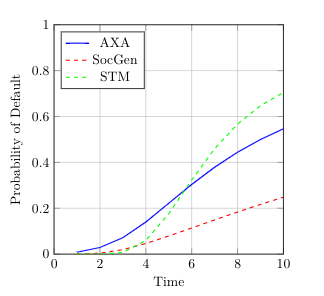

In the paper [Hainaut, D. and Colwell, D.B., A structural model for credit risk with switching processes and synchronous jumps, The European Journal of Finance44(33) (4238):3262-3284], the authors exploit a synchronous-jump regime-switching model to compute the default probability of a publicly-traded company. Here, we first generalize the proposed L\'evy model to a more general setting of tempered stable processes recently introduced into the finance literature. Based on the singularity of the resulting partial integro-differential operator, we propose a general framework based on strictly positive-definite functions to de-singularize the operator. We then analyze an efficient meshfree collocation method based on radial basis functions to approximate the solution of the corresponding system of partial integro-differential equations arising from the structural credit risk model. We show that under some regularity assumptions, our proposed method naturally de-sinularizes the problem in the tempered stable case. Numerical results of applying the method on some standard examples from the literature confirm the accuracy of our theoretical results and numerical algorithm.

翻译:在论文[Hainaut, D. and Colwell, D.B., 《转换过程和同步跳跃的信用风险结构模型》,《欧洲金融杂志》44 (33) (4238) 3262-3284)中,作者利用同步跳跃制度转换模型计算一个公开交易公司的默认概率。在这里,我们首先将拟议的L\'evy模型概括为最近引入金融文献的更一般的温和稳定流程设置。根据由此产生的部分杂交式操作者的独一性,我们提出了一个基于严格正定义功能的总体框架,使操作者非分类化。然后,我们分析了一种基于辐射功能的高效的无网状合用法,以近似于结构信用风险模型所产生的部分杂交式方程对应系统的解决办法。我们表明,根据某些常规假设,我们拟议的方法自然地将缓和稳定案例的问题分解为问题。在从一些标准文献的理论和数字分析结果中应用该方法的量化结果。