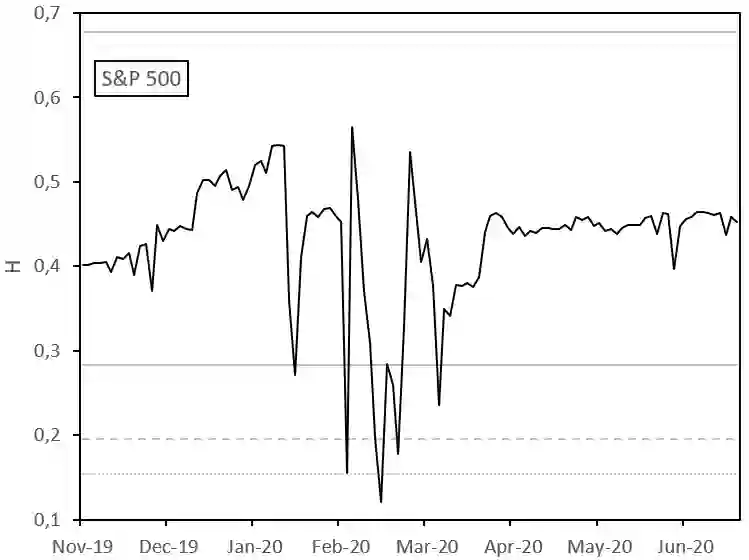

This paper investigates the impact of COVID-19 on financial markets. It focuses on the evolution of the market efficiency, using two efficiency indicators: the Hurst exponent and the memory parameter of a fractional L\'evy-stable motion. The second approach combines, in the same model of dynamic, an alpha-stable distribution and a dependence structure between price returns. We provide a dynamic estimation method for the two efficiency indicators. This method introduces a free parameter, the discount factor, which we select so as to get the best alpha-stable density forecasts for observed price returns. The application to stock indices during the COVID-19 crisis shows a strong loss of efficiency for US indices. On the opposite, Asian and Australian indices seem less affected and the inefficiency of these markets during the COVID-19 crisis is even questionable.

翻译:本文调查了COVID-19对金融市场的影响,重点是市场效率的演变,使用了两种效率指标:赫斯特指数和分数L\'evy-sable运动的记忆参数。第二种方法结合了动态分布模型和价格回报之间的依赖结构。我们为两种效率指标提供了动态估计方法。这个方法引入了一个自由参数,即折扣系数,我们选择这个系数是为了获得观察到的价格回报的最佳阿尔法-sable密度预测。在COVID-19危机期间对股票指数的应用表明美国指数效率的大幅下降。相反,亚洲和澳大利亚指数的影响似乎较小,而在COVID-19危机期间这些市场的效率甚至有疑问。