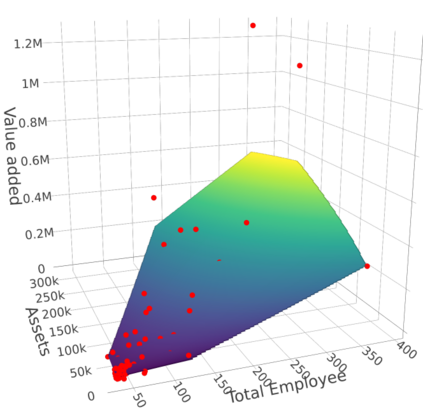

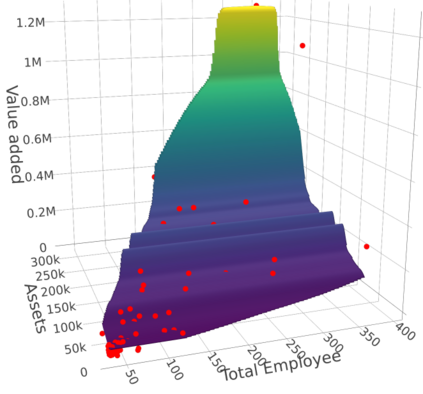

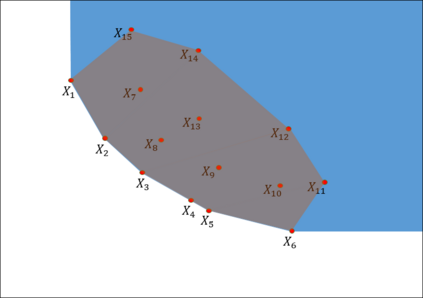

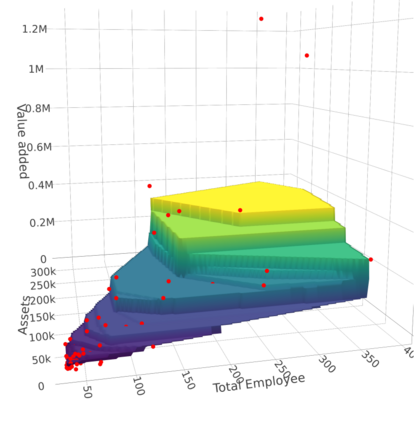

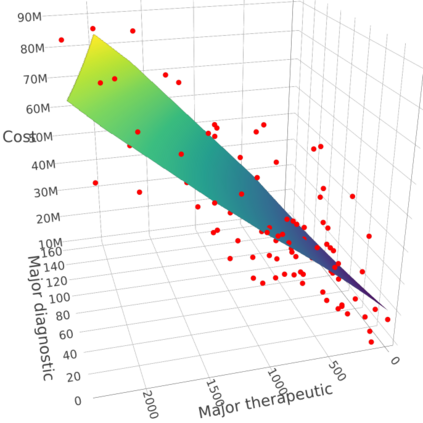

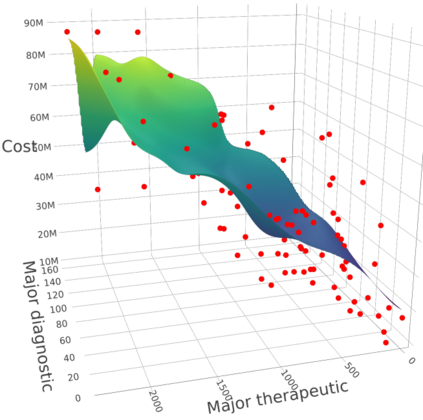

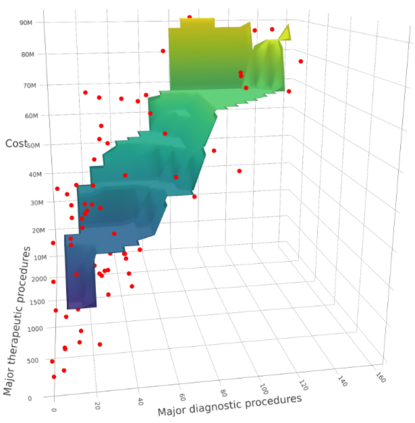

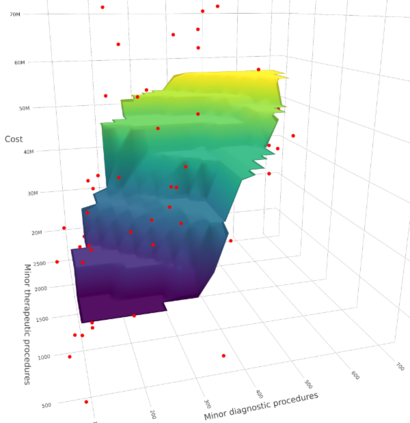

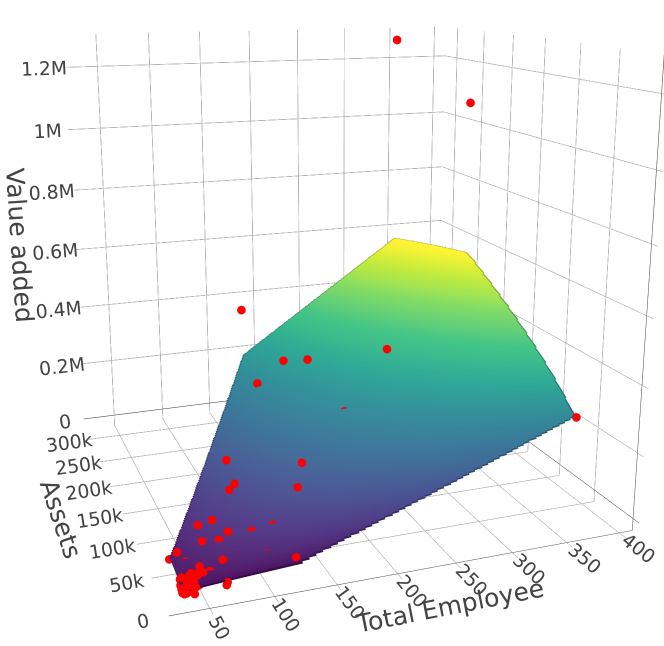

We develop a new approach for the estimation of a multivariate function based on the economic axioms of quasiconvexity (and monotonicity). On the computational side, we prove the existence of the quasiconvex constrained least squares estimator (LSE) and provide a characterization of the function space to compute the LSE via a mixed integer quadratic programme. On the theoretical side, we provide finite sample risk bounds for the LSE via a sharp oracle inequality. Our results allow for errors to depend on the covariates and to have only two finite moments. We illustrate the superior performance of the LSE against some competing estimators via simulation. Finally, we use the LSE to estimate the production function for the Japanese plywood industry and the cost function for hospitals across the US.

翻译:在计算方面,我们证明存在准电流受限最小方形估计仪(LSE),并对功能空间进行定性,以便通过混合整形二次方程式计算LSE。在理论方面,我们通过尖锐的或极分的不平等为LSE提供有限的样本风险界限。我们的结果允许错误取决于共变体,只有两个有限的时刻。我们用模拟来说明LSE优胜于一些相互竞争的估算师。最后,我们用LSE来估计日本胶合行业的生产功能和美国各地医院的成本功能。