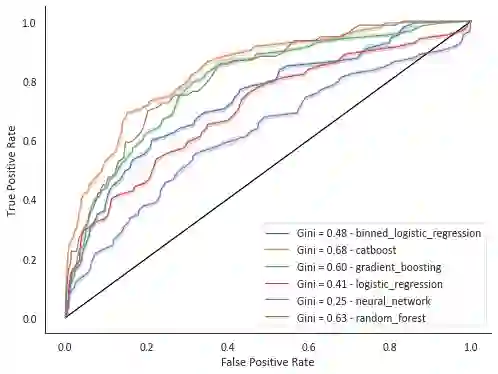

The aim of this project is to develop and test advanced analytical methods to improve the prediction accuracy of Credit Risk Models, preserving at the same time the model interpretability. In particular, the project focuses on applying an explainable machine learning model to bank-related databases. The input data were obtained from open data. Over the total proven models, CatBoost has shown the highest performance. The algorithm implementation produces a GINI of 0.68 after tuning the hyper-parameters. SHAP package is used to provide a global and local interpretation of the model predictions to formulate a human-comprehensive approach to understanding the decision-maker algorithm. The 20 most important features are selected using the Shapley values to present a full human-understandable model that reveals how the attributes of an individual are related to its model prediction.

翻译:该项目的目的是开发和测试先进的分析方法,以提高信用风险模型的预测准确性,同时保留模型解释性,特别是,该项目侧重于将可解释的机器学习模型应用于银行相关数据库,输入数据来自开放数据,在已经验证的全部模型中,CatBoost显示最高性能,在调整超参数后,算法实施产生0.68的GINI。SHAP软件包用于为模型预测提供全球和地方解释,以制定理解决策者算法的人类综合方法。20个最重要的特征是使用Shapley值选择的,以展示一个完整的、可理解的模型,显示一个人的属性如何与其模型预测相关。