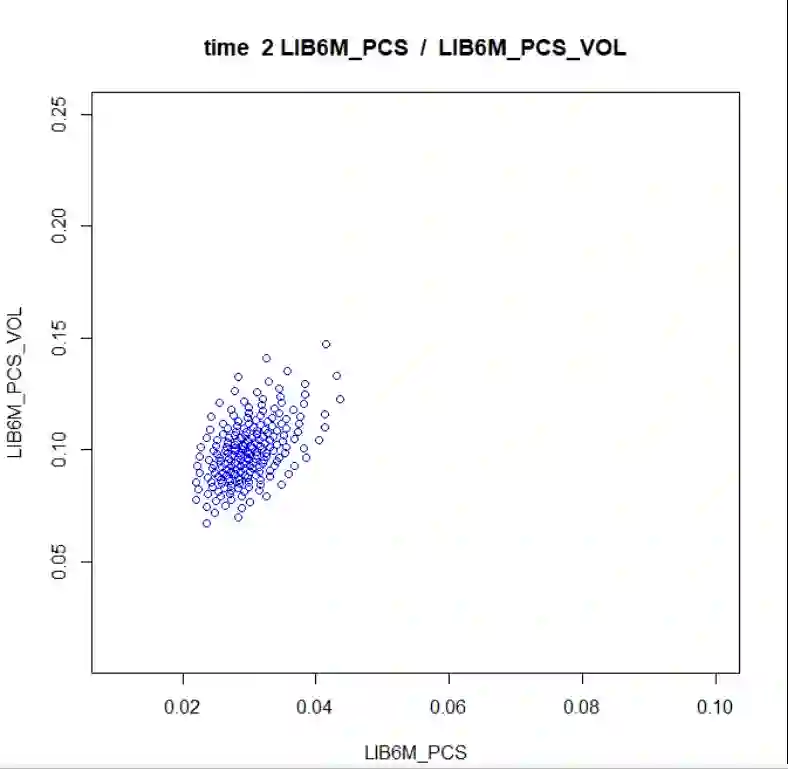

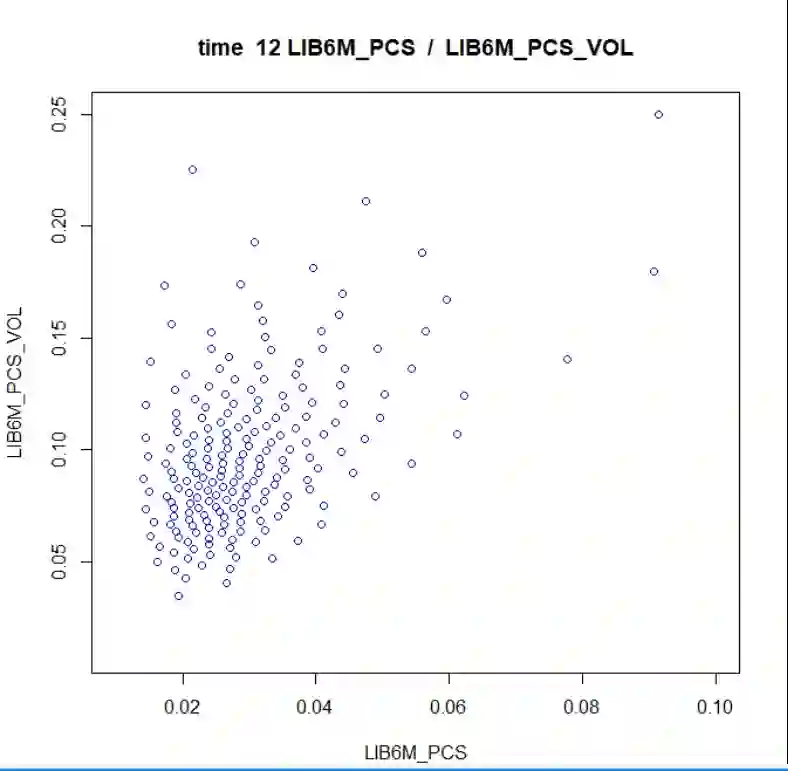

We review a numerical technique, referred to as the Transport-based Meshfree Method (TMM), and we discuss its applications to mathematical finance. We recently introduced this method from a numerical standpoint and investigated the accuracy of integration formulas based on the Monte-Carlo methodology: quantitative error bounds were discussed and, in this short note, we outline the main ideas of our approach. The techniques of transportation and reproducing kernels lead us to a very efficient methodology for numerical simulations in many practical applications, and provide some light on the methods used by the artificial intelligence community. For applications in the finance industry, our method allows us to compute many types of risk measures with an accurate and fast algorithm. We propose theoretical arguments as well as extensive numerical tests in order to justify sharp convergence rates, leading to rather optimal computational times. Cases of direct interest in finance support our claims and the importance of the problem of the curse of dimensionality in finance applications is briefly discussed.

翻译:我们审查了一种数字技术,称为“基于运输的无网路方法”,我们讨论了该方法在数学融资方面的应用。我们最近从数字角度采用了这种方法,并调查了基于蒙特-卡洛方法的整合公式的准确性:讨论了数量误差界限,在这个简短的说明中,我们概述了我们的方法的主要想法。运输和再生产内核的技术使我们在许多实际应用中找到一种非常有效的数字模拟方法,并提供了人工智能界所用方法的一些亮点。在金融行业的应用中,我们的方法使我们能够用准确和快速的算法来计算许多类型的风险措施。我们提出了理论论点以及广泛的数字测试,以证明急剧趋同率的合理性,从而导致相当最佳的计算时间。我们简要讨论了对金融有直接利害关系的案例,以支持我们的要求,以及金融应用中多维度的诅咒问题的重要性。