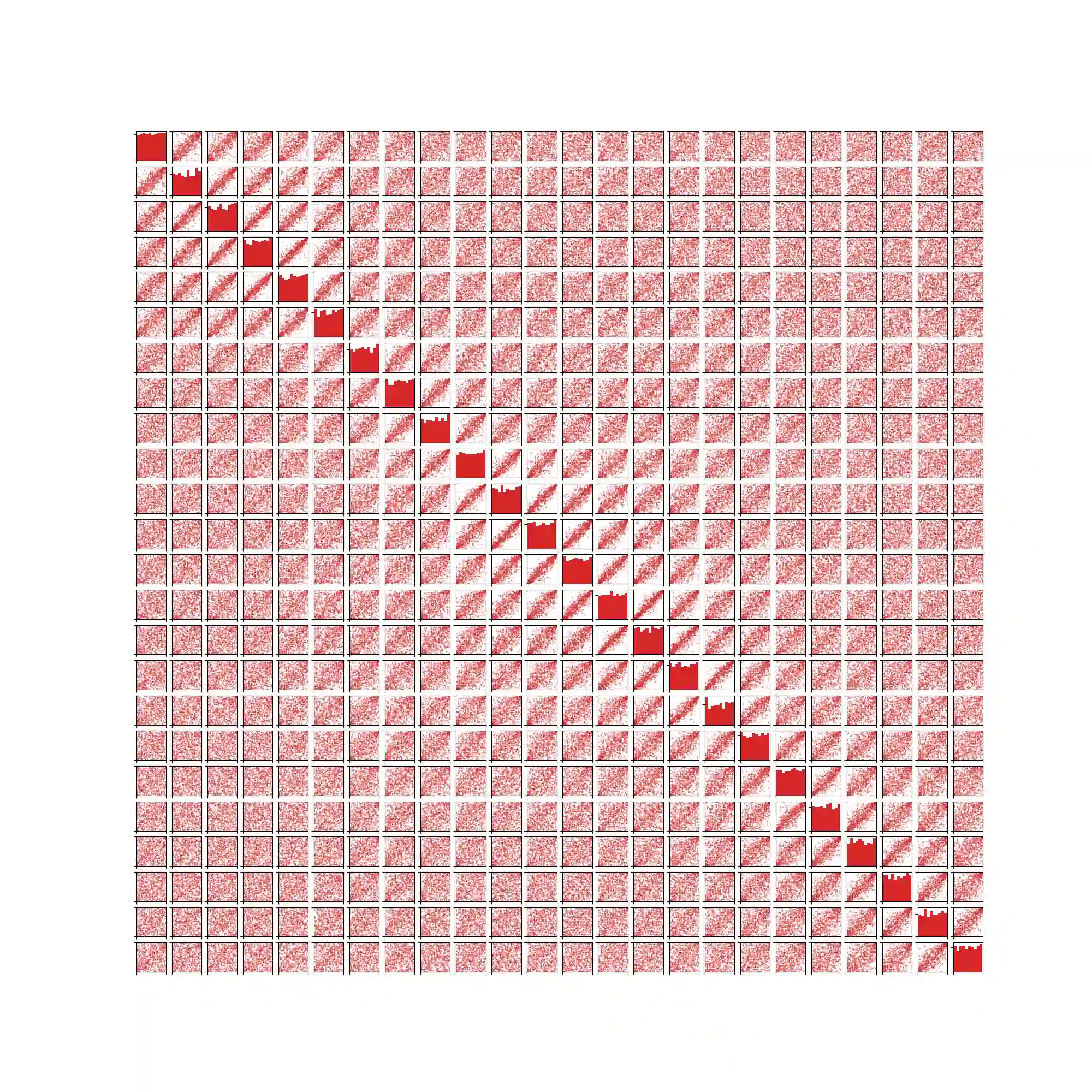

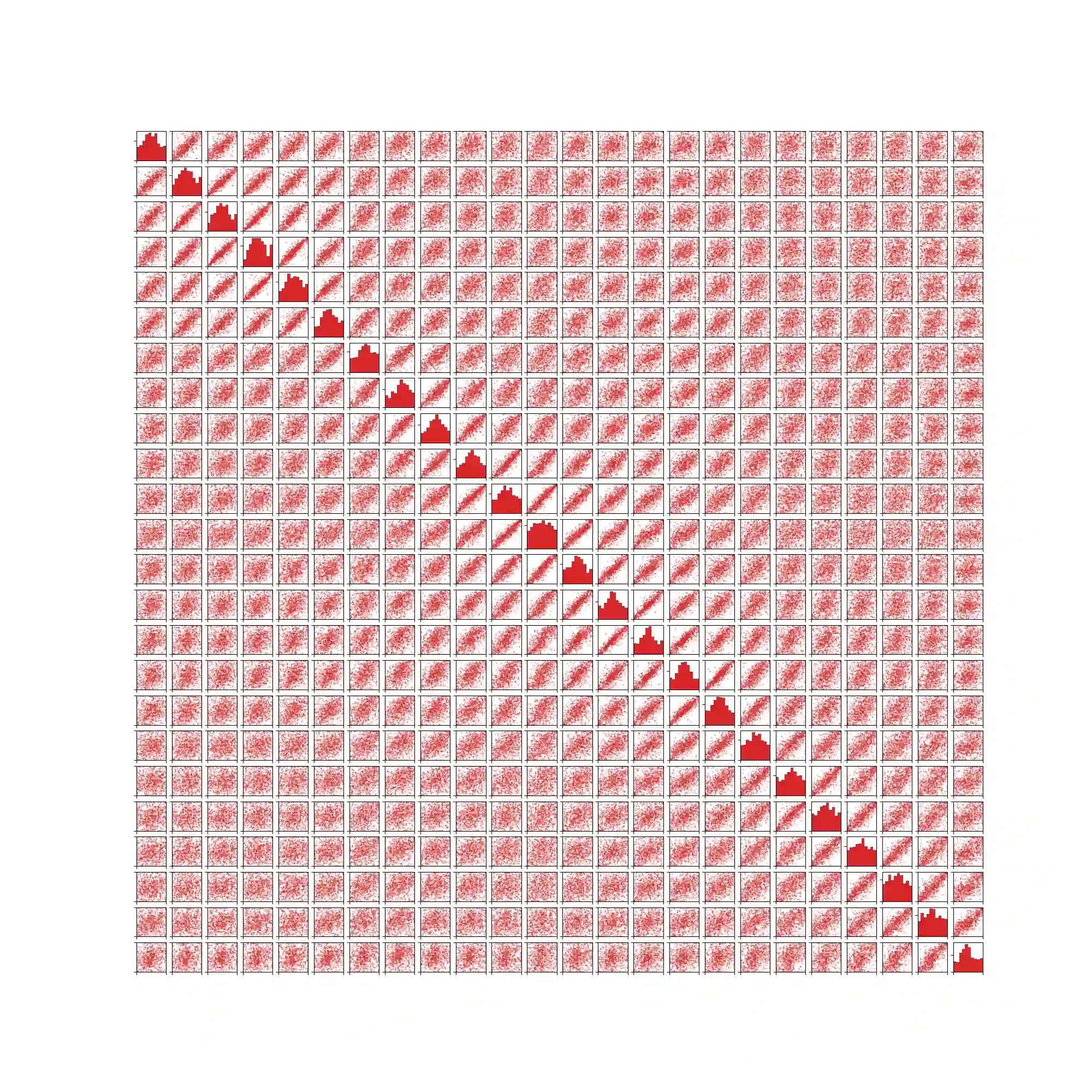

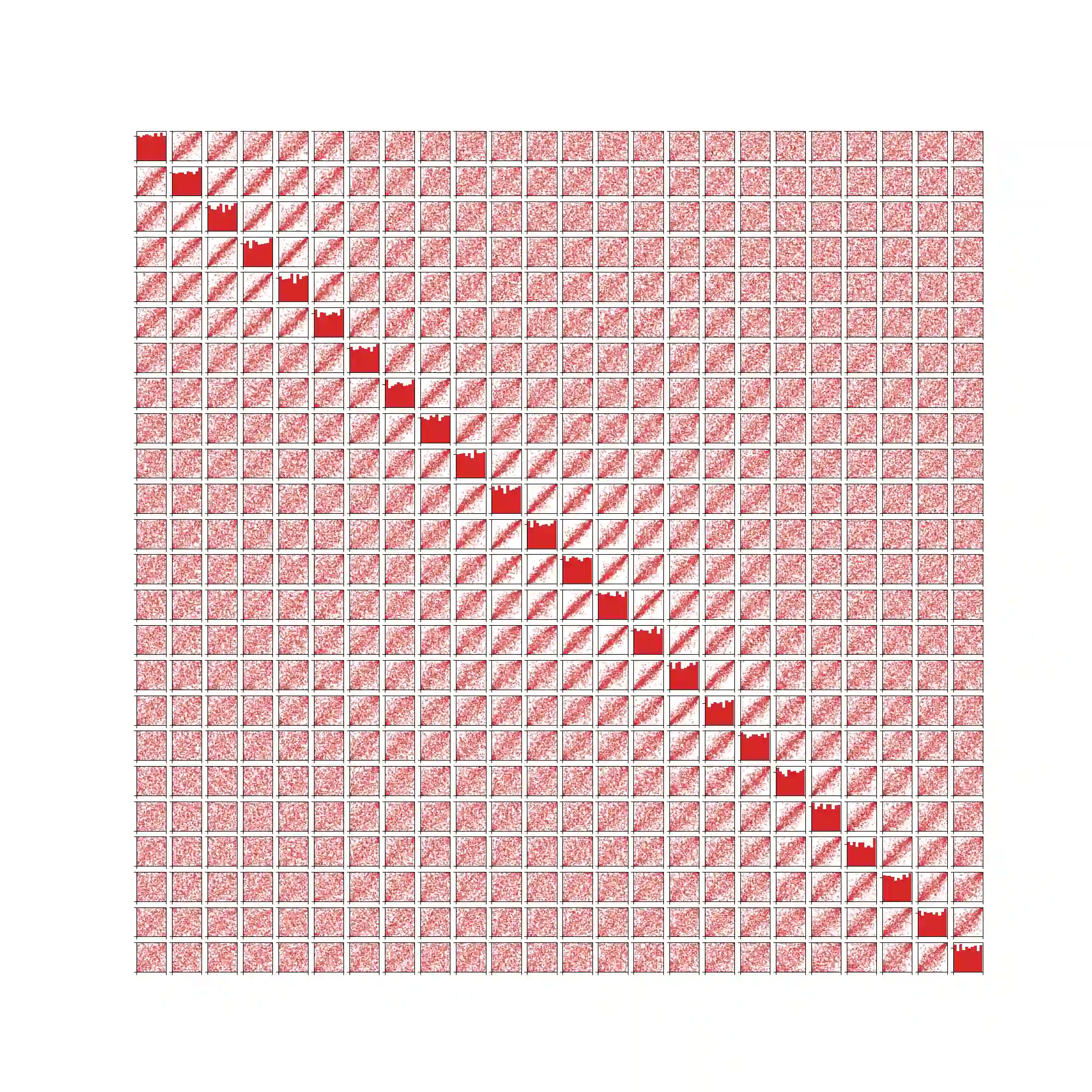

Modeling price risks is crucial for economic decision making in energy markets. Besides the risk of a single price, the dependence structure of multiple prices is often relevant. We therefore propose a generic and easy-to-implement method for creating multivariate probabilistic forecasts based on univariate point forecasts of day-ahead electricity prices. While each univariate point forecast refers to one of the day's 24 hours, the multivariate forecast distribution models dependencies across hours. The proposed method is based on simple copula techniques and an optional time series component. We illustrate the method for five benchmark data sets recently provided by Lago et al. (2020). Furthermore, we demonstrate an example for constructing realistic prediction intervals for the weighted sum of consecutive electricity prices, as, e.g., needed for pricing individual load profiles.

翻译:模拟价格风险对于能源市场的经济决策至关重要。除了单一价格的风险外,多重价格的依赖性结构往往具有相关性。因此,我们提出一种通用的、易于执行的方法,以根据日电价格的单值点预测建立多变概率预测。虽然每个单值预测都指一天24小时中的一个小时,但多变预测分配模式则指不同小时的相互依存关系。拟议方法基于简单的交替技术和一个可选的时间序列部分。我们举例说明了Lago等人(202020年)最近提供的五套基准数据集的方法。此外,我们展示了为连续电价加权总和构建现实的预测间隔的范例,例如计算个人负荷配置价格所需要的预测间隔。